[W]ith Mother’s Day coming up, and Father’s Day soon after, maybe it’s time to have a family discussion about what will happen when the unspeakable happens. Death isn’t pleasant to talk about, but if you’re willing to have that conversation, you’ll make things much easier at a tough time in the future.

No one likes to think about mortality. Young adults consider themselves immortal. Middle agers are fighting the concept of growing older. And the baby boomer generation figures it can bend the rules of aging as it has changed so much of our society in the past 60 years. But sooner or later, our time will come.

Will we leave a giant puzzle for our loved ones and heirs to figure out? Or will we smooth the way to making this transition a bit less painful, leaving them able — and legally empowered — to handle the assets we leave behind?

By the way, this is not a discussion just for aging parents. Families with young children need to organize their finances as well. Who will know the passwords to access everything from bank accounts and 401(k) plans to your valuable cache of airline miles?

Years ago, I created a Personal Financial Organizer form — which is still available free at my website, TerrySavage.com when you sign up for my free newsletter. It comes to you by a link in a return email, and you can print out as many copies as you want, giving them to friends and family to create their own roadmaps to their finances.

This four-page form is used both as a discussion starter and an organizational tool. Once filled out, it serves as a guide to locating your investment accounts, bank and brokerage accounts, will and estate planning documents, cemetery deed, safe deposit box and keys, passwords and credit card account numbers, and myriad other documents that would be hard to find in a crisis or after you’re gone.

But Harris Rosen, a retired executive, has taken it a step further in “My Family Record Book” ($15.95 on Amazon.com). The octogenarian has explained not only what you should organize, but why — and he explains the pitfalls and consequences of not knowing this important information.

Rosen speaks directly to seniors, giving resources and references on everything from how to order a tombstone to services that will take care of your pet after you are gone! There is an entire section on downsizing after the loss of a spouse and advice on how to dispose of furniture and clothing to charitable organizations that will make good use of these items. But mostly he focuses on organizing your financial papers to make life easier for your survivors.

Two other books of a similar genre are the best-selling “Getting it Together” by Melanie Cullen, published by Nolo Press ($14.31 on Amazon), which includes downloadable forms, and the spiral-bound “Peace of Mind Planner” by Peter Pauper Press ($12.04 on Amazon). Both make your planning organized and accessible to family members.

By now you get the idea. Any of these tools will make the perfect gift for the upcoming holidays and provide a starting point for important discussions of end-of-life matters, from locating health care directives and powers of attorney to planning a funeral or finding the policies and assets that will allow the survivors to deal with financial issues.

Yes, it’s a tough subject to tackle on Mother’s Day or Father’s day. But it’s not nearly as tough as it will be to try to figure it out in a crisis when your loved ones are not able or around to help you. And that’s The Savage Truth.

[D]eath and funeral planning are not subjects most people enjoy talking about. Although we know that it will eventually come to us all, it is human nature to avoid discussing our own mortality and it’s easy to convince ourselves that we don’t need to worry until much, much later in our lives.

Sadly, thousands of people die every year without ever making any arrangements for their funeral, leaving grieving families to plan and pay for this without any clear understanding of their wishes.

Why express final wishes?

No one can know exactly when they will die, so taking the time now to talk about your wishes for your funeral makes sense for everyone, whether you are just starting out in life or enjoying a peaceful retirement.

According to a 2015 Comres survey on ‘Public Opinions to Death and Dying’, eight out of 10 British people say they have strong wishes for the end of their life and more than two thirds of us think that if people were more comfortable talking about dying, it would be easier to have our end-of-life wishes met.

The same survey showed that less than 20 percent of us have actually asked our nearest and dearest about their end-of-life wishes.

Graham Jones, director at Sun Life, discussing the insurer’s latest ‘Cost of Dying’ report, said it’s not just details like what flowers to have. “A third of those organising a funeral had no idea whether the deceased would have wanted to be buried or cremated,” he said.

End of life plans and making them known

The reality is accepting that it’s important to have the conversation with your loved ones and knowing how to raise the issue are two very different things. There’s no easy way to say ‘I’ve been having a think about what I want to happen when I die’.

Rather than springing it on unsuspecting family and friends, it might help to raise your own funeral wishes in relation to the passing of a friend or even a celebrity. If you are met with a refusal to discuss it, try to point out that it won’t be any easier if you die without anyone knowing what you wanted for your funeral and beyond.

Talking about dying doesn’t make it happen and can bring peace of mind, allowing us to relax knowing that our plans are understood and, when the time comes, our loved ones will know exactly what to do.

“We all need to get better at discussing our end of life plans, including our funeral plans,” said Claire Henry, chief executive of the Dying Matters Coalition. “It gives us peace of mind to know we’ve made and shared our plans, and it makes life easier for our loved ones to know they are giving us the perfect send-off we want.”

Reduce financial burden and stress by planning ahead

By planning ahead, you can help to ease the emotional and the financial burden on loved ones at a very difficult time. One of the best ways to make sure that your family and friends are not left to pay for your funeral is to consider a funeral plan.

Pre-paid funeral plans make sure you have the funeral you want, planned and paid for in advance. When you purchase your plan, a local funeral director is appointed to take care of your requirements and to make sure that your family receives personal service when it really counts.

A pre-paid funeral plan gives you the opportunity to pre-arrange your burial or cremation, choose your coffin and specify transport. With your wishes laid out and a local funeral director appointed all your loved ones have to do when the time comes is make one phone call to the chosen funeral director.

Save by fixing funeral costs

A pre-paid funeral plan not only gives you control of your funeral arrangements, it also allows you to pay for your funeral director’s services included in the plan at today’s prices despite constantly rising costs.

According to the SunLife Cost of Dying Report 2015, in 2004, the average cost of a funeral was £1,920. Today it is £3,897, and at that rate of increase, in another 10 years, the average cost of a funeral could be more than £7,000.

With a pre-paid funeral, you ensure your wishes are shared with your loved ones and in turn, it provides you with peace of mind that your funeral will not burden your loved ones and guarantees that your funeral director’s costs will be covered, even if you stick around for decades.

[O]lder people who are active investors and who prefer unregulated investments may be more susceptible to investment fraud, a report published Thursday by the AARP Fraud Watch Network found.

The network, established in 2013 to help promote fraud prevention, commissioned a study late last summer that included telephone interviews with 200 known victims of investment fraud and 800 interviews with members of the investing public.

Doug Shadel, lead researcher for the network, said that relatively inexperienced people often invest money on their own these days, in part because of the decline in traditional pensions. At the same time, he said, technology makes it easier for scam artists to reach larger numbers of people, by telephone or email.

The report sought to pinpoint traits that may help explain why some people are more susceptible to investment fraud, Mr. Shadel said. Victims were more likely to be men 70 or older, and they tended to be risk takers. About half of fraud victims agreed that they did not mind taking chances with their money, as long as “there’s a chance it might pay off.”

And nearly half of fraud victims, compared with less than a third of general investors, agreed that “the most profitable financial returns are often found in investments that are not regulated by the government.”

Victims were more likely to report valuing wealth accumulation as a measure of success in life and being open to sales pitches, the research found.

Victims reported that they frequently received targeted telephone calls and emails from brokers and that they made five or more investment decisions a year. Also, they were more likely than general investors to respond to remote sales pitches, including those delivered in television commercials.

As many as 17 percent of Americans 65 and older report being the victim of financial exploitation, according to the Consumer Financial Protection Bureau. Estimates of annual losses are in the billions of dollars. One factor that may play a role is mild cognitive impairment, a condition that can be a precursor to dementia and can diminish an older person’s ability to make financial decisions.

Older people are at risk of being swindled not only by strangers, but also by people they know. Douglas Canada, a 78-year-old retiree in Nevada, sought help from the fraud network after he was tricked by an old acquaintance: He received a call in 2015 from a man who had been a co-worker three decades earlier. The man invited Mr. Canada and his wife to lunch to talk about an investment opportunity. The man and his date sported Rolex watches, and they even bought a diamond ring during the outing. “They really put on a good show,” Mr. Canada recalled.

The man told Mr. Canada that he had grown rich by buying and renovating foreclosed homes in another state. He invited Mr. Canada to invest, promising double-digit returns. Mr. Canada sent a cashier’s check for $40,000 — but has since been unable to contact the man. Mr. Canada has hired a lawyer and a private investigator, and he has written to the state authorities, but isn’t optimistic about getting his money back. “He’s a con man,” Mr. Canada said. “I was gullible, and I fell for it.”

Some scams — gold investing, real estate schemes, and even one involving leases on A.T.M.s — may sound improbable after the fact, Mr. Shadel said, but victims report being persuaded — sometimes, because of word of mouth from friends or family.

Recognizing that you may have a predisposition toward risky behavior, like being open to pitches, may help you avoid being taken in, Mr. Shadel said. “You can at least be aware of your psychological mind-set,” he said. Consumers can take a quiz, based on the study’s findings, on the fraud watch website.

Mr. Shadel urged consumers to deal only with regulated brokers and investments, and to “ask and check”: If you get a call from a broker, ask if he or she is registered with state and federal securities regulators, he said, “and then check to see if it’s true.”

You can check a broker’s background though Finra, the Financial Industry Regulatory Authority, using its online BrokerCheck tool at www.finra.org, or by calling 800-289-9999.

Maggie Flowers, associate director for economic security with the National Council on Aging, said that older people should be skeptical of any offers, particularly unsolicited ones. “Always ask for things in writing,” she said, “so you can think it through and talk through the options with a loved one or peers.”

Here are some questions and answers about older people and fraud: Are older people at risk for fraud only if they are wealthy?

No, Ms. Flowers said. Scam artists know that many older people have fixed incomes, which may make them vulnerable to fraud because they are open to hearing about ways to make money and pay their bills.

Where can I learn more about protecting an older person from fraud?

The National Council on Aging offers tips on avoiding fraud at EconomicCheck.org.

The Consumer Financial Protection Bureau offers a “Money Smart” guide for older adults, and other resources, on its website.

What should I do if I think an older person has been a victim of financial fraud?

You can also contact your local adult protective services agency. You can find a local agency that investigates reports of financial exploitation on the federal Eldercare Locator website or by calling 800-677-1116.

An advance directive is basically just a written document or a series of documents explaining what you want to have happen during your end-of-life care. It may outline a variety of topics, including your wishes for your care, should you become incapacitated, as well as naming proxies and a power of attorney.

These documents will need to be drawn up by attorneys and notarized. These aren’t likely things that you’ll want to have to spend a lot of time dealing with yourself, so it’s common to delegate these tasks to others.

There’s a lot of comfort in knowing that you’ve taken care of everything ahead of time and haven’t left big or stressful decisions to be made after you’re gone. If you’re up to it, it’s important to have legal documents drawn up..

A living will describes the type of healthcare you hope to receive and whether or not you’d like to remain on life support, and under what circumstances, should you become incapacitated and unable to make your own decisions. Living wills can be prepared by attorneys and should be prepared ahead of time.

Last wills are designed to designate property to beneficiaries, assign guardians for minor children, and elucidate any last wishes. This is somewhat different than a living trust, which will transfer property immediately, as opposed to after your death.[3]

In some cases, it may be good for you to delegate these responsibilities instead to a proxy, in the event that you’re unwilling or incapable of making these decisions for yourself. This is often an adult-aged child or spouse, who will be tasked with making choices regarding your health care as things progress.

In some cases, it may be difficult to choose or assign proxy responsibilities to a private party, and you may wish instead to assign them to an attorney. This is extremely common and can be a relatively stress-free way of turning over technical responsibilities to someone else, allowing you to deal with your own comfort and emotional responsibilities.[4]

A health care power of attorney is different than a general power of attorney, which provides for financial assistance after death. While both of these may be appropriate options, it’s important to distinguish between them.[5]

Though it may be slightly unnerving, it’s important to decide what you want to happen to your body after you die. There are many options and considerations, depending on your culture and religious background.

If you want a funeral, or religious ritual to be performed after your death, you may want to arrange the ceremony yourself, or delegate the responsibility to a loved one. Make the arrangements in terms of churches, funeral homes, if it helps you to find closure.

If you want to be buried, decide where you want to be buried and which family members you want to be buried near, if you haven’t made those decisions already. Secure a burial plot by making a down payment, and make arrangements with a funeral home in your area, if necessary.

If you’d like your body to be donated, make sure your donor status is up to date and accurate, according to your wishes. Contact the university or foundation to which you want your remains donated and make the necessary arrangements.

Tomorrow, Part 3 — Making the Most of Your Last Days

After the death of a loved one, you might find yourself overwhelmed with the tasks that need to be done. While your grief can make it difficult to focus on these priorities and take action, there are several things that need to be done immediately after a death occurs, and in the weeks/months that follow. This article offers a simple checklist-style overview for survivor’s to help you prioritize and keep track of what needs to be done after the death of a loved one.

At the Time of Death, Make the Right Call

For deaths that occur at home, it’s important to know who to call. If your loved one is a hospice patient, call the hospice agency to report the death. A hospice nurse will come to the home and pronounce the death. The nurse might also call a mortuary for you and arrange for pick up of the body.

If your loved one is not a hospice patient, then you must call emergency services to notify the local police or sheriff of the death. A coroner or medical examiner might also be required at the scene if the death was sudden or unexpected.

Contact a Funeral Home

Whether a hospice nurse makes the call or you call yourself, a funeral home must be contacted to arrange for pick-up of the deceased’s body. If funeral arrangements have been made in advance of the death, all you will need to do is confirm the arrangements with the funeral director. If no funeral arrangements were made in advance, you will need to begin planning a funeral.

Determine if your loved one made any arrangements for a funeral or memorial service. If he or she did not make any advance arrangements, then begin to plan the funeral or memorial service. You might want to call on relatives or close friends to assist in making these arrangements. More »

Contact Attorney, Accountant and/or Executor of Estate

Contact Employer (if applicable)

Ask about any outstanding compensation due. Find out whether dependents (if any) are still eligible for health and/or insurance benefits and whether there is a life-insurance policy through the company.

Contact Social Security

Contact Social Security and any other agency that might be making monthly payments to the deceased. The Social Security Administration (SSA) phone number is 1-800-772-1213 (TTY 1-800-325-0778) or you can visit the SSA website for more information. Find out if survivors are entitled to any further benefits.

Contact the Veterans Administration

If your loved one served in the Armed Forces, the Veterans Administration (VA)might offer benefits for funeral or burial costs. Stop any monthly payments that the VA might be paying the deceased.

Examples of assets include life-insurance policies, bank accounts, investment accounts, real-estate ownership, retirement accounts, business ownership, etc.

Liabilities might include mortgages, owed taxes, credit-card debt, unpaid bills, etc.

Inventory and Distribute Personal Belongings

You might want the help of family members and/or close friends for this task. Determine which of the deceased’s belongings to keep, which to distribute to family and friends, and which to donate or sell.

A patient at Houston’s Ben Taub Hospital waits on a stretcher in the hallway for space in the emergency room to open up.

Doris Portillo keeps the door to her father’s old room closed to avoid remembering the last few months of his life. It’s a small room, barely large enough for a bed, a small bureau, and a television, all of which are long gone. This is where she, her siblings, and her nephew cared for her father, Aquilino Portillo—feeding him, lifting him out of bed to take him to the bathroom, doing their best to clean the sores that festered beneath his weight.

A naturalized citizen from El Salvador, Portillo brought her parents to the United States in 2001 and sponsored their green cards so that she could take care of them as they aged. In late 2013, when Aquilino was diagnosed with end-stage metastatic prostate cancer, she discovered how difficult taking care of him would be.

Portillo’s insurance through her employer—she works nights cleaning offices for the City of Houston—didn’t cover her father, and the family couldn’t afford to buy insurance for him. They tried to determine if he could qualify for Medicare, the federal health benefit for the aging, or Medicaid, the state-run health insurance for the poor, but were given conflicting responses depending on whom they talked to. Confused by the requirements and limited by her poor English, Portillo applied for Medicaid for her father, but never got a response. So, for the better part of a year, the Portillos carted Aquilino back and forth to the emergency room in a wheelchair, where they would wait for hours, sometimes all night, simply to have his pain medications refilled.

As Aquilino’s condition worsened, he could no longer be moved from his bed to see a doctor. His body was riddled with tumors. His legs became too heavy for him to move, and his pain became unbearable. “It was ugly, ugly and scary, to see a loved one dying,” Portillo says in Spanish. “And if that person is your father, it’s something indescribable.”

By the time Portillo found out about a small county program that sends health workers to the homes of low-income, bedridden patients, her father had been at home without pain medication for two and a half months. The nurse practitioner who came, spurred by Aquilino’s obvious suffering, rushed to order medication to make him more comfortable. Two days later, when the morphine had barely had a chance to soothe him, he was gone.

“Sometimes people die and death is sweeter,” Portillo says. “I don’t think death is ever sweet, but they suffer less. My father suffered so much, he really fought to leave us.”

Portillo is not alone. Some 28 million people in the United States do not have health insurance, and for the dying and their families, lack of insurance is devastating. Though the care needs that arise with terminal illness are simple, they are often prohibitively difficult to meet without insurance. The uninsured and their families are left to navigate public and charity end-of-life care options that vary widely across the country, if they are available at all. There are no data on how or where the uninsured access this care, and the scope of unmet need is virtually unknown. What is known is that, at the end of their lives, many uninsured people quite literally cannot afford to die with dignity.

* * *

For the most part, patients with insurance have a choice when they receive a terminal diagnosis. Some choose to exhaust all possible avenues for fighting their disease, hoping conventional treatments or experimental drugs will prolong their lives. But when treatment fails or its toll is too great, the quality of a person’s final months or weeks often matters more than prolonging them. Doctors tend to steer those patients toward hospice, the holistic form of palliative care that focuses on treating symptoms in order to make a patient more comfortable and functional as they near death.

One of the fundamental tenets of hospice care is that patients and their families will have a better experience of death if the patient dies at home, among loved ones and familiar surroundings. The actual care is fairly simple, and focuses on managing symptoms and making the most of the time the patient has left. Family members administer most of this care, with support from the hospice team (a doctor, nurses, and often a social worker, chaplain, or volunteers), whose oft-repeated motto is to “care for the caregivers.”

Hospice began on the fringes in the 1960s and ’70s, somewhat at odds with the American medical-industrial complex. Hospice for Medicare-enrolled adults can’t begin until curative treatment has been abandoned, something that’s difficult for many patients, their families, and even their doctors to do. But hospice has gained a mainstream foothold over the last few decades, as doctors and patients have increasingly accepted that “life-extending” treatments can make dying more painful, often with little or no benefit to the patient. The vast majority of hospice recipients—about 85.5 percent—access the service through Medicare, and the proportion of Medicare beneficiaries using hospice before they die has more than doubled since 2000. The Centers for Medicaid and Medicare Services recently began reimbursing doctors for time spent explaining the benefits of hospice to their Medicare-funded patients, further encouraging hospice advocates, who see a lack of awareness as the fundamental barrier preventing patients from getting good end-of-life care.

But what about the millions of uninsured poor Americans who simply have no way to pay for that care? While Medicare, Medicaid, and most private insurers cover hospice, millions of Americans—mostly working-pooradults under 65—don’t have access to an insurance program. In most of the 19 states that have not accepted the Affordable Care Act’s Medicaid expansion, for example, qualifying for Medicaid is almost impossible unless you’re a child, pregnant, a parent on welfare, elderly, or disabled (only Wisconsin is finding ways other than the federal expansion to cover its childless adults). In these states, more than 3 million adults fall into what’s called the ACA “coverage gap”: They don’t qualify for Medicaid under the states’ rules, but make too little to qualify for federal subsidies on the government-run insurance marketplaces. To put this in perspective, in order to qualify for those federal subsidies, a household has to make at least 100 percent of the federal poverty level—about $20,000 a year for a family of three.

The country’s 11 million undocumented immigrants face particularly high barriers to accessing health care, including hospice, as they are legally barred from enrolling in any federally funded insurance program. Some 63 percent of the undocumented population goes without insurance coverage, and studies show that they tend to seek health care less in general, partly due to fears that interacting with any authority could lead to deportation.

Today, more than 76 percent of hospice patients are white, and terminally ill patients are less likely to die at home the lower their incomes. In many poor urban communities, less than 5 percent of the dying receive hospice care in the last six months of life.

Public-health systems around the country are trying to address these disparities, and Harris County, where Aquilino Portillo lived, provides a stark example of just how difficult it is for local safety nets to fill this care gap. Texas has the highest rate of uninsured residents in the country, with nearly 1 million uninsured people in Harris County alone—roughly 22 percent of its population. For employed adults under 65, that number is closer to 30 percent. The Houston area has an expansive health-care safety net that serves the poor, including many private hospitals and clinics that provide some care for free. But it’s the county’s taxpayer-funded hospital district, Harris Health, that is ultimately responsible for providing healthcare to those who can’t afford it. Like many public-health systems around the country, it struggles to handle its uninsured population while simultaneously facing perennial budget problems, due in part to the chronic poverty of its patients. Difficult decisions must be made and priorities set; only so much can be done to care for the dying when so many others need treatment.

Harris Health doesn’t offer hospice, but it pieces together something similar through in-hospital consultations, a palliative-care clinic, and the house-calls program that Doris Portillo found too late. Low-income patients can use these services with financial assistance from the county, which used to come in the form of a laminated “Gold Card,” a name that locals still use to refer to the benefit. But applying for this financial assistance takes precious time—Doris Portillo says she spent a month away from her job trying to get her father Gold Card eligibility—and many people eligible for the benefit are not able to use it. While low-income undocumented immigrants in Harris County are entitled to Gold Card assistance, for example, providing proof of residence and income to establish eligibility can be difficult, since they often share housing and work as day laborers for cash. It’s an unspoken truth in Harris County that the hospital district serves those who can pull together the correct documentation to prove their eligibility for financial assistance, those who can endure the system’s chronically long wait times, and those who can essentially coordinate their own care. Like the Portillos, many end up getting end-of-life care the only way they know how—at the emergency room.

Dr. Ricardo Nuila, a hospitalist at Ben Taub, the largest of Harris Health’s three hospitals, describes the county’s emergency rooms as a kind of revolving door for terminally ill poor people. The uninsured tend to find out about serious illnesses like cancer later than the insured, since they use primary health care less frequently and are twice as likely to postpone or go without medical care due to cost than those with insurance. This means that by the time many uninsured patients seek care, their symptoms are acute and require immediate attention in an emergency room. But even those in non-emergency condition simply see no alternative to the ER—federal law requires emergency providers to stabilize a patient’s symptoms regardless of his ability to pay. Once that’s done, the patient is usually sent home; for terminal patients, this cycle only repeats as their condition worsens.

“That’s one of the most concerning things when you’re working in the hospital and you walk through the emergency room,” Nuila says. “The patients might actually have their pain and their suffering well controlled with medications at home, but they’re in the emergency room just to get prescriptions.”

Emergency rooms are brutal places for the dying. Patients and their families can spend entire days waiting to be seen by a doctor. In 2013, a local news channel reported 14-hour wait times at Ben Taub, with as many as 100 people at a time filling the reception area. Terminally ill patients must describe their symptoms again and again as they pass through various levels of triage, often undergoing tests or procedures intended to lay the groundwork for treatment they know is futile. Once admitted to the hospital, they are disturbed every couple of hours by nurses checking vital signs, even if the patient has only hours to live. There are the sounds and smells of other patients, and the comings and goings of a legion of hospital workers. “You’re dying in a semi-public place,” says Nulia. “That can be very difficult for somebody who’s trying to have an environment of respect for their dying one.”

Hospitalists like Nuila try to send terminally ill patients home with as much medication as possible and some sense of how to keep their symptoms at bay. The textbook next step for insured patients, he says, is to suggest hospice so that families can get the proper care at home. But he knows that many of his patients can’t afford it. “In a way, we’ve just sort of come to accept poor outcomes for unfunded patients,” he notes. “We just say, ‘OK, let’s hope that they get hospice services, or charity hospice kicks in.’”

According to the National Hospice and Palliative Care Organization, only around 1 percent of hospice services in the United States are delivered free of charge to families who otherwise have no way to pay for them. Nonprofit hospice centers are often required to provide some charity care, but there are no government guidelines as to who should receive it or how much of it should be available in a given geographical area. One-fifth of all hospices nationwide provide no charity care.

Nuila estimates that Ben Taub is able to connect unfunded patients with charity hospice only about half the time, though Harris Health doesn’t officially keep track of that number. It is rare for charity care to be flat-out unavailable, but for indigent terminally ill patients who often have only days to live, the wait time—commonly four to six weeks—is as good as nothing. When they can’t get a patient into hospice, the already overworked doctors, social workers, and case managers at the hospital do their best to piece together the next-best thing.

Alexie Cintron is one of those doctors. A palliative-care specialist who provides serious-illness consultations for hospitalized patients at Ben Taub, he also runs an outpatient palliative-care clinic for patients who are staying at home. Provided the patient is covered by a Gold Card and can make it to the clinic to see him, Cintron can show family members how to care for their dying loved one and send them home with equipment like a hospital bed or a bedside commode, and they can get prescriptions filled through the system’s own pharmacy at Ben Taub.

“Essentially, I’m kind of a hospice doctor by default,” Cintron says. “We can’t find them hospice, we don’t provide hospice as a system, and so I’m the fallback.” But the help that Cintron provides is a far cry from the comprehensive and consistent care provided by hospice, and he and the nurse practitioner he works with can stretch their time only so far. “Many times we struggle with being able to support the family enough so that we try to keep this patient from bouncing back to the hospital in the next week or so.”

For poor families, the difficulty of providing good care for their loved one often stretches far beyond the health-care system itself. “If they have to take three different buses in order to get to our clinic, they might not be able to make it in time [for an appointment],” Cintron says. Money is often an issue—even with financial assistance from the county, which can lower the cost of filling a prescription to as little as $8, some people are unable to afford their medicines. Then there’s the scarce resource of time. Family members have to take off work or find child care, and they must make time to keep appointments, get prescriptions filled, and apply for financial assistance. This is all before they’ve spent any time actually caring for their dying loved one.

For at least some indigent patients, however, Harris Health does provide something akin to hospice care in the home. Dr. Anita Major is director of the system’s geriatric house-calls program, the one that was able to visit Aquilino Portillo only once before he died. The service began in the 1980s, but has expanded its patient load fourfold since 2010 in an effort to address the need for home care in the community. It’s not hospice, she says—partly because it generally involves less frequent visits, less comprehensive support, and only serves patients who are unable to leave their homes for medical appointments—but it’s pretty close. Like many uninsured people, however, Major’s poorest patients often connect with home care only when their illness has reached a crisis point and the extremity of their symptoms requires hospitalization anyway. “The problem is we meet them and, you know, 10 days later they’ve died,” Major says. “And we really should have met them a year before that.”

But the most vulnerable population, says Major, are those who never cross paths with the system—people who may be eligible for county health services but don’t know it or can’t access them. For every family like the Portillos, who find care too late, there are likely many more who never find it at all. “I think it’s a lot more than I’m aware of,” says Major. “Those are the people that I think really are suffering, and they’re just invisible to us.”

* * *

Nationwide, it is hard to say just how many people who want or need end-of-life palliative care are forced to go without it. One recent nationwide survey assessing the availability of palliative care in general (including for nonterminal patients) showed that, while the prevalence of palliative programs in hospitals is steadily increasing, fewer than half of the country’s rural or isolated hospitals offer the option at all, let alone to unfunded patients. Statistics on hospice itself are generally tracked through utilization by Medicare and Medicaid beneficiaries, and there is no database for how or where the uninsured access the service.

“It’s difficult to measure unmet need,” says Carol Spence, vice president for research and quality at the National Hospice and Palliative Care Organization. She adds that quantifying hospice access is complicated by its elective nature. “There’s not a defined population that should have hospice like there is for a given illness,” she says. “Hospice is a choice.” But it’s a choice many of the dying poor don’t have.

For safety-net providers, expanding access to hospice is not a simple question of funding the service itself. Though outpatient hospice services cost on average 15 times less than treating the dying in a hospital—between $100 and $200 per day for hospice versus close to $3,000 per day in a Texas public hospital—offering hospice through public systems like Harris Health would actually increase the overall cost to those systems. Public hospitals tend to have far more demand for care than they can meet, so a bed vacated by a patient transferring to hospice will immediately be filled, and the hospice patient’s care will amount to a new expenditure. Like many public-health systems around the country, Harris Health is facing a deficit this fiscal year—$8 million—even after cutting overtime for its staff and reducing the number of people who qualify for Gold Card assistance. Because these systems are struggling to fund even their preventive care, adding to their deficits to treat the already dying is simply not an option.

The underlying reality is that local safety nets can only be expected to do so much for America’s uninsured, whose real problem, especially at the end of life, is that they don’t have insurance. According to the National Hospice and Palliative Care Organization, the most efficient way to increase access to hospice for low-income patients is to provide insurance coverage to the nation’s 28 million people who currently don’t have it. “It’s better to insure people ahead of time than to subsidize safety-net care after the fact,” insists Charles Begley, a veteran health-care researcher at the University of Texas School of Public Health. “There are many very valuable, very important, very cost-effective health-care services that this limited, publicly funded health-care system cannot address.”

Not only would insurance allow indigent patients to use the same hospice providers as the more well-off, but the consistent access to primary care that comes with being insured would make them more likely to hear about the service and choose to use it earlier in their illness. At the same time, Begley adds, insurers would have a financial incentive to make hospice a more visible and readily available option throughout the health-care system. Safety-net providers could focus their resources on acute and preventive care, and everyone would be better off.

But the United States is a long way from providing insurance to all. Four of the five states with the highest uninsured rates have decided not to expand their Medicaid programs under the Affordable Care Act, or even to set up their own insurance exchanges. According to the Kaiser Family Foundation, nearly 5 million more people nationwide would qualify for Medicaid—and gain access to hospice coverage—if their states chose to expand. If Texas were to expand its Medicaid program under the ACA, it would bring in nearly $6 billion in new federal funding and insure 2 million low-income adults, nearly 400,000 of them in Harris County alone.

In the current political climate, however, that seems unlikely to happen. Texas and the other eighteen states that have refused to expand Medicaid coverage currently rely on temporary federal funding to reimburse their safety net systems for the uncompensated care of uninsured patients. While half of Harris Health’s $1.3 billion budget comes from county property taxes, for example, about a quarter of it comes from these reimbursements. (Harris Health’s palliative-care services, including the house-calls program, were either created or expanded to their current level using this funding.) US Health and Human Services Secretary Sylvia Burwell has made it clear that while the federal government won’t punish states for not expanding Medicaid, it does expect them to come up with a viable long-term alternative in return for continued funding. Policy-makers in Texas, as in other Republican-controlled states, claim they merely want the freedom to design their own indigent-care systems without federal constraints, but the Texas legislature has made no move to put a long-term strategy in place. Analysts like Begley believe that lawmakers are waiting for the results of the 2016 election to determine their next moves—and in the meantime, safety-net funding is far from secure.

The election could, indeed, be a turning point. Donald Trump, the presumptive Republican presidential nominee, has vowed to repeal the Affordable Care Act—a move that health-policy experts warn would reverse the real progress the law has made in insuring low-income Americans. The Democrats would do the opposite: Presumptive presidential nominee Hillary Clinton plans to expand the ACA toward a goal of universal coverage, while Bernie Sanders proposes placing all Americans and undocumented immigrants under a federally administered, single-payer healthcare program.

“This is another make-or-break election for the Affordable Care Act,” said David Blumenthal, president of the Commonwealth Fund, a health-care research foundation, addressing a conference at the Harvard Law School in January. At the same time, he added, “we are now, for the first time in a generation, actively debating how far left to go with health-care policy.”

But until that debate results in tangible changes in how the health-care system works, the burden of caring for those who are dying in poverty will remain mostly on the shoulders of families like the Portillos, who simply do what they can to ease their loved one’s pain when the system isn’t there to support them.

“Of course,” says Portillo, “there is another way.” And, of course, she’s right.

When it comes to the end of life, hospital stays are more intensive and more expensive than alternatives.

People who die in the hospital undergo more intense tests and procedures than those who die anywhere else.

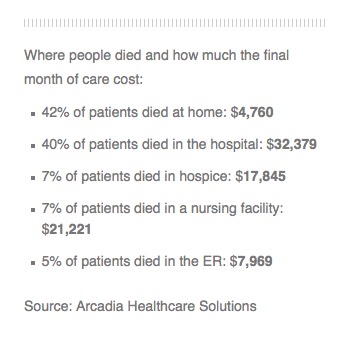

An analysis by Arcadia Healthcare Solutions also shows that spending on people who die in a hospital is about seven times that on people who die at home.

The work confirms with hard data what most doctors and policymakers already know: Hospital deaths are more expensive and intrusive than deaths at home, in hospice care, or even in nursing homes.

“This intensity of services in the hospital shows a lot of suffering that is not probably in the end going to offer people more quality of life and may not offer them more quantity of life either,” says Dr. Richard Parker, chief medical officer at Arcadia.

Arcadia analyzed all the Medicaid claims data for a private Medicaid insurance company in one Western state and detailed how many billable medical procedures each patient received and where. Patients in hospitals were billed for far more medical interventions in the last days of their lives than people who died in other settings. The company declined to name the state or company.

The study showed that 42 percent of patients died at home at a cost of about $4,760 for their last month of life, while 40 percent died in a hospital at a cost of $32,379. Dying in a nursing home was the second most expensive locale, inpatient hospice was third and an emergency room was fourth.

“In the end, everyone died. They all died,” Parker tells Shots. “If we look at this retroactively, retrospectively — and we could go back and ask people — I bet most of them would say I’d rather be home with my family.”

Parker says the cost of hospital deaths paid for by Medicare or private insurance are likely even higher because they pay doctors and hospitals more for their services.

Many studies have shown that people, when asked, say they’d prefer to die at home rather than in a hospital. However, those wishes aren’t always realized if a person hasn’t given clear instructions to a doctor or family member.

Parker says hospitals are designed to cure people who are ill rather than to allow people to die peacefully.

“The culture of American medicine today and for the last several decades is to keep treating patients regardless of the quality of life,” he says. “A lot of physicians have been reluctant to admit that the patient’s life is coming to an end.”

The picture is more complicated than the data show, says Dr. Lachlan Forrow, a professor of medicine and medical ethics at Harvard University.

Many patients move from home to hospice to hospitals and back during the last 30 days of life. And some may end up in the hospital because their pain or symptoms weren’t adequately controlled at home.

Still, he says, hospitals are just not good at caring for dying people.

“We do lots of very expensive things in hospitals to people in the last part of life who would rather be home, and we do those in part because in the hospital they get paid for,” he says.

It’s the only way to justify keeping in a hospital the people who need around the clock nursing care but can’t get it at home.

“If we really tried to make sure people at home could have what they needed at home, we could take better care of them, with less medical system-caused suffering, at lower cost, sometimes much lower cost,” he says.