In the realm of financial planning, agents and advisors diligently guide their clients through the complexities of retirement savings, investments, and insurance. Yet, there’s a critical aspect that often doesn’t receive the attention it warrants until it’s too late: the cost of dying. Recent data reveals a stark reality: The price tag attached to end-of-life care and funeral expenses is climbing, propelled by inflation and escalating health care costs. Let’s look at the implications of these rising costs and outline strategies financial professionals can employ to assist their clients in preparing for the future.

The unavoidable cost of dying

The Consumer Price Index indicates a notable 4.8% increase in funeral costs over the past year, signifying the upward trajectory of end-of-life expenses. An average American now faces more than $24,000 in medical and funeral costs at life’s end. Specifically, end-of-life medical expenses average more than $16,000, while the median funeral cost nears $8,000. These figures highlight an uncomfortable truth: even in death, one cannot escape the financial implications of inflation.

Deepening funeral costs

The average funeral in the U.S. costs between $7,000 and $12,000, encompassing expenses from caskets and embalming to transportation, plots, flowers, services, headstones and funeral home fees. Opting for more elaborate services or higher-end options can significantly inflate these costs. This financial burden is not one most individuals wish to impose on their relatives posthumously.

The true ‘killer:’ Medical care costs

Although funeral expenses are steep, the cost of medical care in the final stages of life is even more daunting. Medicare provides some relief but hospital, palliative care and hospice care costs continue to surge. Hospital stays can exceed $10,000 per day before insurance. Despite a preference for dying at home, only about 25% of individuals do so, with the majority ending their lives in some form of medical care facility.

Planning for estate and legal considerations

Beyond medical and funeral costs, there are estate and legal fees to consider. The process of settling an estate and distributing inheritances involves a complex web of legalities, adding another layer of expense that can easily propel total end-of-life costs beyond $50,000.\

Strategic planning for end-of-life expenses

Savings and investments. One approach is for clients to allocate a portion of their savings or investments specifically for end-of-life expenses. This proactive measure can mitigate the financial impact on loved ones.

Insurance solutions. Life insurance or specialized end-of-life insurance products can offer a safety net for funeral and other final expenses. However, seniors may face high premiums, and those with existing life insurance policies may be overinsured if they plan to use these funds solely for funeral costs.

Life insurance settlements. For seniors facing steep life insurance premiums or those with more insurance coverage than necessary, a life insurance settlement presents a viable option. Selling their policy in the secondary market can provide them with a lump sum to cover end-of-life expenses, freeing them from the burden of escalating premiums.

The role of agents and advisors

Financial professionals play a pivotal role in navigating these complex waters. By conducting policy appraisals, advisors can determine whether a life insurance settlement is appropriate, potentially reallocating those funds toward long-term care insurance or directly covering end-of-life expenses. This strategic planning can alleviate the financial strain on clients and their families, ensuring a more manageable and dignified end-of-life experience.

As the costs associated with end-of-life care continue to rise, agents and advisors are tasked with a crucial responsibility: to help their clients plan comprehensively, considering not only the joys of retirement but also the inevitable costs of dying. By exploring all available options, from savings and investments to insurance products and life insurance settlements, financial professionals can guide their clients toward peace of mind for themselves and their loved ones. Inflation may be an unyielding force, but with thoughtful planning and strategic advice, navigating the financial aspects of end-of-life can be less burdensome, allowing individuals to focus on living their final days with dignity and grace.

Today’s topic: How do you talk to your parents about death and finances – without seeming like you are money-hungry?

Daughter wants to avoid repeat hardships after dad’s death

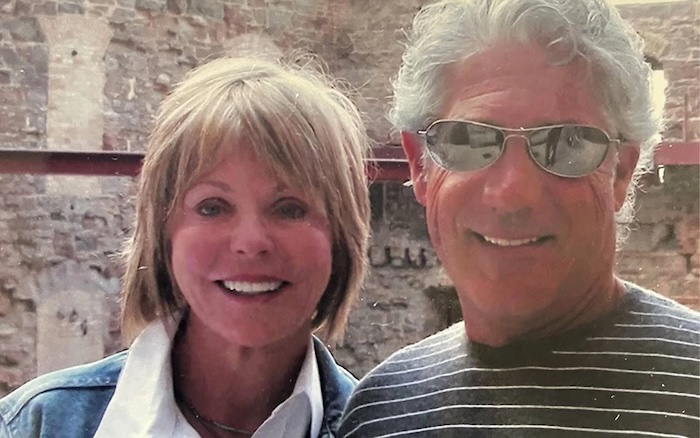

The dilemma: Last year, Melisa Gotto’s father died.

“We did talk about death and sort of what accounts he had and what his desires were for when he passed, but we didn’t really get into the nitty-gritty of it,” said Gotto, of Green, Ohio.

But Gotto said she – and her father, Dave, – were unprepared for all that came with tying up everything from funeral arrangements to his financial affairs.

Melisa Gotto, right, said she was not prepared to handle financial for her dad, Dave Gotto, right, left after his death. Having the uncomfortable conversation about his finances and wishes would have helped, she said.

For instance, her dad had a burial plot in California but died in Nevada. She didn’t know it cost $10,000 and required special health department permission to transport a body over state lines.

Gotto’s parents were divorced. Now, Gotto wants to avoid the headaches and heartache she dealt with after her dad’s death. She has begun talking to her 69-year-old mom, Kim Slingluff, about how Slingluff will afford to live the rest of her life – and how the two of them prepare for her mom’s death.

“It is a very uncomfortable conversation when you start talking about a taboo topic,” said Gotto, CEO of Scandal Co-Active, a boutique public relations and marketing agency. “As a society, we don’t really talk about death, but it’s something that we all will experience. I think it’s something we should all start talking about.”

Gotto’s dad had communicated verbally that she’d be the executor of his estate when he died. But he left no other instructions for her and her brother, such as his medical wishes or details of what exactly to do after his death.

“He was pretty organized and had everything in a safe, but I didn’t know where that was,” she said.

Melisa Gotto, left, said she was not prepared to handle financial affairs for her dad, Dave Gotto, at right, after his death. Having the uncomfortable conversation about his finances and wishes would have helped, she said.

Gotto said her dad also didn’t have enough finances to cover his funeral expenses. And seven months after his death, she’s still trying to get the title for his car.

Gotto says she doesn’t want to seem greedy discussing her mom’s finances or wishes after her death, but she doesn’t want to repeat what happened with her dad.

She has begun telling friends with kids to “do them a huge favor. Get all of this settled before you get older because it’s so important.”

Gotto said she has been approaching the subject with her mom with compassion and empathy. Slingluff has been verbally telling her things, but Gotto knows she needs to get things in writing.

Melisa Gotto, right, is having the uncomfortable conversation about death and finances with her mom, Kim Slingluff, left, to avoid similar hardship she faced after her dad’s death.

Gotto’s advice to others: “Make a list of everything you want to ask them because you don’t want to have to keep revisiting the conversation.

“Try to have some patience and understanding. And then if they don’t want to have those conversations, you have to respect that, too.”

Don’t leave grieving relatives with a mystery to solve

The expert advice: Talking about death and finances is an uncomfortable conversation and one that some of certified financial planner Jan G. Valecka’s clients are more willing to have than others.

Some clients feel “they have to disclose everything: their bank accounts, how much … they have, and that’s where I think it becomes uncomfortable and they feel a little bit vulnerable,” said Valecka of Valecka Wealth Management in Dallas.

“If I had to talk to somebody about estate planning, financial planning, legacy (planning), I would start from the benefit of your loved one. ‘Who would you want to take care of or help if all of a sudden something happened to you? … And it doesn’t have to be dollar signs, it just has to be more of what are your wishes,” said Valecka.

Having that conversation and letting your loved one know where the important documents are can be so helpful after a death, she said.

Valecka’s family had its own experience with this subject. Her husband, Bob, knew that he would be the executor of his uncle’s estate. However, his uncle did not want to discuss details of his death or his financial affairs.

Bob Valecka’s uncle, Joseph Valecka, was found dead the day after Christmas in 2022, with his wife who has dementia next to him unaware that he had died.

Bob and Jan Valecka had to quickly work to gain guardianship of the aunt and tend to the uncle’s estate.

But they had no instructions. They couldn’t find a will or any estate documents. It turned out there had been a will and Power of Attorney and other documents drawn up. They didn’t find them until after they went to court for emergency guardianship of the aunt.

Bob Valecka, left, knew his uncle, Joseph Valecka, wanted him to be executor of his estate after his death. But his uncle left no instructions, including whether there were any estate documents.

The unanswered questions ranged from the significant to the mundane. Had he wanted to be buried or cremated? The uncle and aunt had a lake house. But the Valeckas had no key and didn’t know the security code to get into it, or how to turn on the wells, or if someone plowed the driveway.

“It was a mystery to us,” she said. “It could have been so much easier with planning and an uncomfortable conversation.”

Gotto’s approach to talking to her mom with compassion is a good one, said Valecka.

Some people are just uncomfortable talking about their death, she said. Some clients say it makes death too real.

Approach your loved one with the idea that they are sharing their wishes and helping the people they love after their death, Valecka suggested.

In that conversation, talk about getting a will, health directives and even user names and passwords for digital accounts, she said. Valecka didn’t know she would need a copy of the uncle and aunt’s marriage license to get the aunt on the uncle’s Social Security benefits. Valecka has now added that to her estate documents.

Organizing and clearing out an entire home is not most people’s idea of a good time. Doing so while grieving compounds that sense of dread and overwhelm. So perhaps it’s a bit of a surprise that The Gentle Art of Swedish Death Cleaning, Margareta Magnusson’s 2017 book chronicling her approach to ordering an estate in the wake of a loss, was a smash success. Her humorous, accessible guide amassed a cult following among an audience of fans that grew even larger after Peacock released its eight-episode series of the same name last year. But because both the book and the show it inspired tackled an issue that most people will encounter—and one that’s often swept under the proverbial rug—perhaps it’s not all that surprising that consumers found themselves clamoring for more content on post-loss decluttering.

Public meditations on grief and discussions around it seem more easily broached following the COVID pandemic, which spurred a reckoning in how we deal with mourning. The years since 2020 have been characterized by plenty of discourse on grieving, Zoom grief groups, and other bereavement support efforts, opening the floodgates on conversations that might have struck folks as morbid prior but now feel decidedly necessary to have out in the open. Podcasts like Anderson Cooper’s All There Is serve an audience of those looking to reflect on loss and how to live afterward. In cleaning out the New York City home of his late mother, the celebrated designer and socialite Gloria Vanderbilt, Cooper was guided by a number of handwritten notes Vanderbilt left like breadcrumbs to help him along. “These are Daddy’s pyjamas,” read one dispatch on a piece of paper near a pair of satin trousers.

Family portrait of the Coopers as they play on a sofa in their home, Southampton, Long Island, New York, March 30, 1972. American author and actor Wyatt Emory Cooper and heiress Gloria Vanderbilt Cooper sit with their sons, Carter (1965 – 1988) and Anderson Cooper.

Not everyone is given such clear direction in how to sort through a loved one’s dwelling after their passing. AD caught up with some experts on the subject, including a professional organizer, the owner of a liquidation and clean-out service, a death doula, and Magnusson herself, to advise on how to face the inevitable task—which all our pros say can, and should, be put into practice before a loss occurs. “Start before you are too old, or too weak, or get that final diagnosis,” Magnusson tells AD. “The upside is a better, easier life in which you don’t have to worry about the people you leave behind and all your crap they have to go through.”

How do I clear out a house after someone dies?

Both Magnusson and Mark Ferracci, owner of the Central Maryland–based clean-out and liquidation service Sanford & Son Estate Specialists, say that age 60 is the time to start organizing the objects of your estate for those who will someday have to clear it all out.

Allie Shaw, a professional organizer operating in the Greater Toronto area, recommends starting off by taking inventory of all the important items inside the abode, including anything of sentimental value (like photo albums, beloved heirlooms, or official documents) or monetary value (such as jewelry or china). When her own mother was given months to live, she became Shaw’s first client. Over 10 months, Shaw and her mother “had lots of conversations, going through possessions room-by-room and item-by-item,” she says. “It was very cathartic and it was a time in my life that I was so grateful for. She often said, ‘I got more months because we had this time.’”

In conversations about death and estate organizing it may go without saying, but Shaw encourages having formal documentation in place, like a will indicating your wishes for certain belongings. Though the act of preparing a will and even death cleaning an abode while the resident is still alive and well might feel bleak to some people, it’s important to remember that setting things in order can alleviate major stress later down the line. “It is a monumental task and often people think they’re leaving everything behind as a gift, when I’d say most of the time it’s a big burden,” Shaw explains.

Consider what you can manage and when to call in the estate cleaning pros

There’s no rule of thumb to tell whether your particular estate will need a whole team of professionals to clean out. But whether it’s a small apartment or a sprawling mansion, clearing a loved one’s spaces after they’ve died is rarely a one-person job. Particularly for those who value sustainability and cringe at the thought of wasting the beloved items of a family member’s residence, estate clean-out services like Ferracci’s might be the way to go as they’re plugged into the proper channels to help prevent waste. His team is trained to recycle materials, to facilitate the sale of pieces that have value, and to donate items that no longer have a place with the deceased’s family members before resorting to the dumpster.

Like a number of estate clean-out services, Ferracci’s process begins with a simple conversation—an informal chat for which he doesn’t charge that takes place in the abode. “I always say the same thing to people: Get the personal stuff out, get the financial-related stuff out, get the family mementos out; things that you want, those are key,” he says of his preliminary discussions with clients. Making sure family members have combed through the residence for items they hold dear so that all that’s left are things they won’t mind parting with is crucial. “Before I come in to do the job, I want to know that all that stuff’s gone and that everybody’s picked through it.”

How much does it cost to hire professionals for estate cleaning? And how long will it take?

The cost of an estate clean-out varies by how large the home is, which determines how big of a crew the service will need and how many days to allot for the project. A typical family home will likely take two to three days for Ferracci’s team to process, and he estimates that 90% of his average clean-outs cost between between $2,500 and $5,000. His team will sometimes purchase items to sell from clients’ estates, which can help offset that cost: “One [clean-out] I just started, I quoted them $4,400. I gave them $800 for the contents and the price was $3,600, and I’ll be there about two and a half days.” Condos and smaller spaces will generally cost less, while hoarding situations as well as larger abodes drive the price tag up. Though it’s not the norm, Ferracci has encountered homes where the bill was as high as $20,000 to clean everything out.

If you’re coming at an estate clean-out from the “gentle” perspective, meaning you have time to get things in order while the resident is still with us, an organizer may be the way to get things going gradually. As Magnusson advises, “death cleaning is for the living.” Shaw says that in her experience, organizers will charge $50 to $100 an hour. The process usually takes place across several sessions of two or three hours each in order to get a sense for the volume and how much accounting there is to do.

How can I deal with the death-cleaning process while grieving?

Getting ahead of organizing and cleaning a home before a loss takes place is ideal, but that’s just not always possible. It’s likely that the majority of people faced with clearing out a loved one’s estate are still in the grieving process. Even when it’s not a full estate but rather a few rooms with the deceased’s items, the emotional weight can be heavy. Magnusson found clearing out her husband’s spaces in their shared home after his death, particularly his clothing, was “the saddest thing I have ever done.”

Some mourners seek the services of a death coach or death doula to help them navigate the complex emotions that surface during grieving. The process of estate cleaning, which can be stressful under any circumstances, is particularly difficult after a loss. New York City–based death doula Mangda Sengvanhpheng knows that there’s no official guidebook to navigating loss, but when it comes to sorting through the ephemera of a loved one’s life, it’s helpful to have a group of helpers around: “Whether that is with your family members, your loved ones, friends, doulas, therapists, whoever it is that can become a support team, find those people to help you move through that,” she suggests.

Parsing through the objects of a deceased family member’s home can often make for bitter fighting between relatives, something both Ferracci and Sengvanhpheng have experienced in their work. Whether or not there are fights over which items go to whom or which things should be kept versus which should be tossed, finding difficulty in the process of going through these items can be viewed as a microcosm for grief in general. For certain things from an estate that we simply have no place for, it’s ultimately about acknowledging that love and value and then letting go.

“An object is an object, right? A table is a table. But these things have meaning because we imbue meaning in them,” Sengvanhpheng says. “There are stories in the objects, there are memories in the objects. When we lose people, as irrational as it may feel, there’s a reason for [feeling tied to objects]. We lose someone physically and these items—something tangible from them that we’re holding onto—mean so much.”

Parting with a loved one’s things can feel like a jarring reality check in the wake of a loss. Sengvanhpheng’s work involves trying to reframe that: “Letting go of items can be a form of acceptance,” she says. “If, for example, your sister takes something from your mother’s estate that you wanted, you can acknowledge that and then find ways to accept that this is just the reality. How can we start letting go? We consider how you can connect to your mom in a different way.”

Sometimes, there’s a melancholy beauty about ushering these emotionally charged objects into their next phase and assigning them a new narrative. Grief coach Charlene Lam curated an art show on the experience of going through her mother’s home and the objects she decided to keep and discard. When Shaw was taking inventory of her mother’s estate, she happened upon a beautiful rocking chair that had a long history in the family and was very beloved to her mother. They landed on donating it to the local library so that generations to come might make good use of it. “It’s still there and they love it,” she says.

Delaying the death-cleaning process can end up costing you

For many people in the golden years of their life, Ferracci’s seen enough to recommend downsizing when a large family home no longer serves your needs. He’s met clients who have proclaimed that their parents’ move from a big house to a smaller condo in their twilight years was “the best thing they’d ever done”—giving them ability to travel, save money, and ease the burden of sorting through a massive house for their children when that time came. When elderly homeowners aren’t capable of maintaining their houses, issues like accumulated clutter, mold, rot, and overgrown yards can make for an especially pricey clean-out and can even cause the home’s value to go down.

For those looking to list the family home after clearing it out, delaying on a needed clean-out runs the risk of confronting a more difficult selling market later down the line. “You’re going to continue to do the maintenance and you continue to pay the bills for the house, and the house is vacant, and interest rates can start to go up,” Ferracci says. He’s dealt with clients who struggled to sort through items or found themselves in gridlock with family members about what to do with the estate, ultimately leading them to list the residence many months later for thousands less than if they would have been more efficient in the clean-out process.

Ultimately, your pace is your choice. How to prepare for a loss, or even your own death, is not something AD purports to have all the answers on, but dealing with the items of our lives is manageable with the proper tools, outlook, and support. “We are all dying,” Magnusson says. “This is not morbid. It is just fact. Take care of it.”

We’re all going to die, and before that, we will probably navigate the deaths of several people we love along the way.

Too dark? Discomfort with the idea of death may be the reason that people rarely talk about it, plan for it, or teach each other how to cope with it.

“Many people in our society are death phobic and do not want to talk about it,” said Marady Duran, a social worker, doula, and educator with the International End-of-Life Doula Association. “Being an end-of-life doula has been so much more than just my bedside experiences. I am able to talk with friends, family, and strangers about death and what scares them or what plans they have. Being a doula is also about educating our communities that there are many options for how end-of-life decisions can be made.”

When you or a loved one inevitably faces death, there can be an overwhelming feeling of What do I do now? What do I do with these feelings… and all this paperwork? End-of-life doulas (also called death doulas or death coaches) are compassionate and knowledgeable guides who can walk with you through death and grief.

The experience of supporting a childhood friend through her death at the age of 27 motivated Ashley Johnson, president of the National End-of-life Doula Alliance, to commit herself to this role.

“Walking alongside her during her journey, I recognized the tremendous need for education, service, and companionship for individuals and their families facing end-of-life challenges,” Johnson said. “The passing of my dear friend only solidified my commitment to this path. I saw it as my calling to extend the same level of care and support to others who were navigating the complexities of end-of-life experiences. I firmly believe that every individual deserves the dignity of a well-supported end-of-life journey, and that starts with demystifying the process, reducing fear, and helping families achieve the proper closure they need to heal.”

What to expect from a death doula

The services provided by an end-of-life doula are actually pretty varied and flexible. Much like birth doulas, they do not provide any medical care. These are some of the services Johnson said she provides in her work:

Advance health care planning. This might include a living will, setting up durable power of attorney for health care, and advance directive decisions. “We help individuals and their families navigate the complex process of advance healthcare planning, ensuring their wishes and choices are respected and documented,” Johnson said.

Practical training for family caregivers. End-of-life doulas can teach caretakers and family members how to physically care for their loved ones as they near death.

Companionship to patients. “We provide emotional support and companionship to patients, helping to ease their feelings of isolation and anxiety,” Johnson said.

Relief for family caregivers. Caring for a dying family member can be relentless, but caregivers need time to step away and care for themselves too.

Creating a plan for support at the patient’s time of death. A person nearing the end of their life may be comforted by many things in their environment, from the lighting, music, aromatherapy, and who’s present. A doula can help coordinate all the details.

Grief support. “Our role extends into the grieving process, offering support to both the dying person’s loved ones and the patient during the end-of-life journey and beyond,” Johnson said.

Vigil presence for actively dying patients. “We ensure that no one faces the end of life alone by being a comforting and compassionate presence during the active dying process,”Johnson said.

Help with planning funeral and memorial services. Planning services is a complicated task to tackle while you are likely exhausted with grief. Doulas have been through this process many times and can be a steady hand while you make decisions.

“Our aim as death doulas is to enhance the quality of life and death for all involved,” Johnson said. “We provide a range of non-medical support, fostering an environment where individuals and their loved ones can find comfort, guidance, and a sense of peace during this profound and delicate phase of life.”

When is it time to bring in a doula?

Death doulas can provide comfort and support to both the dying person and their loved ones at any stage of the process. They can step in to help before, during, or after a death.

At any time, before you even receive a terminal diagnosis, doulas can help you prepare emotionally and practically with planning for end-of-life wishes, advance care planning, and creating a supportive environment.

During the end-of-life phase, doulas are more present to offer emotional, spiritual and practical support. They may be available weekly or daily, as needed.

After death, doula services continue for the family of the deceased.

“There really is no timeline for grief,” Duran said. “Some will want to meet one or two times after the death, and some do not want to do grief work at all. It is a personal journey, and some people may take years to do the work.”

Support for an unexpected death

Not all deaths come with an advanced warning or time to prepare and plan. Even in the case of an unexpected death, an end-of-life doula can help you handle practical details and process grief. They can:

Provide emotional support

Help you understand the grief process

Teach you coping strategies

Help with arrangements, legal, and financial matters

Help you create meaningful memorial rituals to honor the deceased

Provide connection and community

Listen and validate your feelings

Provide long-term support

“My mentor Ocean Phillips, who is also a doula, always reminds me that ‘grief is another form of love,’” Duran said. “Grief gets a bad rap, and many people do not want to feel grief, but it can be transformative for many who experience it. People who go through an unexpected death of a loved one may feel guilt—‘If only I…I could have…’ The doula can hold space for them and allow them to share that. We can never fix or change, but we can stand with them and provide loving kindness along the way.”

Other professionals to help you navigate a death

Death doulas work in conjunction with many other professionals, including healthcare workers and hospice staff, to help families go through the process of death and all that follows.

“The whole team has a piece in being able to connect with those navigating grief and death. I always recognize that I am just one small part of the larger community that will help support those facing death and loss,” Duran said.

These are a few other professionals you might want to reach out to when facing the death of a loved one:

It’s been nearly five years since Pat Miles’ husband, Charles “Bucky” Zimmerman, died at age 72 after a short bout with pancreatic cancer. He was healthy, she says, so his illness came as a shock. Another unwelcome surprise? What happened after his death.

Instead of being able to grieve fully, Miles was consumed by attorney battles, tracking down account numbers, and sorting through investments. She says it was a “nightmarish” scenario where the people she thought were on her side weren’t interested in her well-being. The retired, award-winning Twin Cities TV anchor and radio host, who now lives in Arizona, was truly lost when it came to navigating her husband’s death and consumed by what she calls the “grim fog of grief.”

“If you wait until someone’s sick and dying, you’ve waited too long because you’re not going to get the information you need at that point.”

“Bucky and I had a will and a trust – I thought everything was taken care of,” Miles, 73, says. “As it turned out, nothing was taken care of. If you wait until someone’s sick and dying, you’ve waited too long because you’re not going to get the information you need at that point. You’re thinking about keeping this person alive for another day or getting them to drink a bottle of water. You’re not thinking about the account numbers, the investments, the other things you don’t know about. If you don’t do all these things when times are good, you’ll have a tough time, just like I did.”

“The people who have read the book tell me they are taking action,” Miles says. “They’re making changes. They’re dealing with it. They’re thanking me for writing and speaking about this. That’s very gratifying

Turning Anger Into Action

Miles listened to hundreds of people tell their stories during her journalism career. But the experiences people tell her about now hit differently than during her time as a broadcaster.

“I tell people I used to be like you. I never would have come to listen to me talk about this book.”

“When I sign books after a speaking engagement, everybody has a story to tell me, and I’d say 90% of these are not good stories,” says Miles, who has talked to many different groups, including major financial institutions, since the book’s release. “It had me reliving a lot of it. They say my mom went through this; my mom had this happen. As a culture, we don’t want to deal with death. I tell people I used to be like you. I never would have come to listen to me talk about this book.”

Writing “Before All Is Said and Done” was anything but a cathartic experience. However, Miles doesn’t think of it as a “sad” book but an informational one.

“I was motivated to write the book because I got extremely angry – at myself and Bucky,” she recalls. “It was pure anger at being stupid and naive. Bucky died, assuming everything was going to be fine. He said I wouldn’t have to worry about anything. That wasn’t true.”

The Power of Preparation

Miles has seen first-hand how powerful it is to be prepared for death. Her co-author, Suzanne Watson, took all the advice they collected for “Before All Is Said and Done,” including changing her and her husband’s estate plan and checking in with a financial advisor. When Watson’s husband recently died, she was able to fully grieve his loss without worrying about the things that Miles struggled through.

“It gave her peace of mind because she was so prepared,” Miles says. “That’s why I wrote the book; this doesn’t have to happen to you if you educate yourself. I’ve started preparing for my death. My kids will have all the information they need when I’m gone. It’s like any other fear — you must face it. That fear starts to go away because you’re dealing with it.”

“You need someone to walk alongside you. There are many good people out there, and I wish I would have met them earlier.”

Many families avoid conversations about death because they’re uncomfortable. Miles addresses this theme throughout the book, including in the chapter “Dad Never Told Us That: The Quandary of Stepchildren.”

“It causes families to split up and siblings never to speak again,” she says. “It doesn’t have to be that way if we just take the time to communicate and properly prepare.”

She recently had a conversation with a woman whose husband was in a coma. Her stepchildren had power of attorney, changed everything, and left the woman with nothing. But her husband eventually recovered, found out what happened, and made sure his wife would be well taken care of in the future.

“If her husband hadn’t woken up, she said she would have been living in her car,” Miles recalled.

Surrounding Yourself with Allies

When she started researching the book, Miles scoured the internet for resources. She found things about grief, estate planning, and wills, but there was no what she called “How to be a Widow for Dummies.” As she dug into her project, she was surprised at the universal themes surrounding death.

“The most amazing thing is that every single person I talked to had issues – financial, attorney, family, stepchildren,” she says.

“We plan for everything in our lives — a big wedding, a baby’s birth. Death is a big event, too,” she continues. “You need to plan for this event as much as you plan for anything else in your life because it will happen to 100% of us. Dying is a very lucrative business, and the people in it want to make money, and they will make money off you if you don’t know what you’re doing.”

Miles advises people to assemble a team of trusted advisors, including a friend to take with you to meetings. She wishes she would have listened more carefully when she and Zimmerman met with financial experts and lawyers because once he died, she was on her own.

“You need someone to walk alongside you,” she says. “There are many good people out there, and I wish I would have met them earlier.”

The Little Things

Even a recent trip to a warehouse club store reminded her that there are still so many things she doesn’t know even after writing her book. When she went to renew her membership, which was in her late husband’s name, the employee helping her commented on all the rebates that come with the card. Miles was dumbfounded.

“It was in his name, but my card has my picture on it,” she says. “I didn’t get any rebates for five years. It’s stuff you don’t know. Even the little things.”

Miles doesn’t hesitate to answer when asked what she thinks Bucky would feel about all she’s done since his death.

“He’d be extremely proud,” she says. “He always was very proud of me. Bucky loved to have his picture taken, and he loved to have people talk about him. I think he’d be very happy about all of this.”

No one can predict exactly how long you will live with cancer, whether you have metastatic stage 4 disease (cancer that has spread to distant organs) or a less advanced stage. No matter where you are in your cancer treatment, end-of-life planning can ease some of the burden on you and your loved ones. If you take time now to reflect on your wishes, you can increase the chances you’ll achieve the outcomes you want.

Soon after any cancer diagnosis is a good time to consider end-of-life planning. Your doctor can answer questions about your prognosis, including what the realistic options are and what those treatments can achieve, says Steven Pantilat, MD, the chief of the division of palliative medicine at the University of California in San Francisco.

Laura Shoemaker, DO, the chair of palliative and supportive care at Cleveland Clinic, adds, “Care planning, ideally, is about planning for the entire trajectory of the illness, including but not limited to end of life.”

This can be done at any time and should be tailored to your needs.

Reflect on Your Values, Priorities, and Wishes

This reflection process can be difficult to initiate, but will be well worth it. It should include talking with your family, caretakers, or even a counselor.

“Each person’s plan will be a reflection of their lives, values, and personal priorities,” says Kate Mahan, LCSW, an oncology social work counselor in the Canopy Cancer Survivorship Center at Memorial Hermann the Woodlands Medical Center in Houston.

“It is often helpful to think of this as a series of discussions instead of a single talk,” she adds. “While we all know that no one lives forever, it is often very challenging to consider our own mortality.”

End-of-life planning allows your healthcare team to understand what matters most to you, says Mohana Karlekar, MD, the section chief of palliative care at Vanderbilt University Medical Center in Nashville, Tennessee.

It’s important to think about expressing your end-of-life wishes in writing if your cancer has progressed, or you’re experiencing more complications from your treatments.

This may be the time to ask yourself where you would prefer to spend your final days — for instance, at home or in a hospice house, says Eric Redard, a chaplain and the director of supportive care at High Pointe House, part of the Tufts Medicine Care at Home network, in Haverhill, Massachusetts.

Do you want to accomplish anything special? Is there a meaningful place for you to visit while you’re still mobile? “The list is endless,” says Redard.

Appoint a Decision-Maker

By communicating openly with your healthcare team, you can make more informed choices about the medical care you want if the time comes when doctors and family members have to make decisions on your behalf.

One of the most important end-of-life decisions for any person with a cancer diagnosis involves selecting someone who will be a voice for you when you can’t speak for yourself.

“Ask yourself, who would I want to make decisions for me? Anyone with cancer could — and should — do that,” says Dr. Pantilat.

Your choice can be enforced through a durable power of attorney for healthcare. It’s a type of advance directive, sometimes called a “living will.” This document names your healthcare proxy, the person who will make health-related decisions for you if you can’t communicate them to your providers.

Write Advance Directives

Outline your wishes in advance directives. The following are decisions you may want to consider including in these documents, says Redard.

Tube feeding Nutrients and fluids are provided through an IV or via a tube in the stomach. You can choose if, when, and for how long you would like to be nourished this way.

Pain management It’s helpful for advance directives to include how you want the healthcare team to manage your pain. You can request as much pain-numbing medicine as possible, even if it makes you fall asleep, or just enough to reduce pain while allowing you to remain aware of the people around you.

Resuscitation and intubation You may decide that a do-not-resuscitate (DNR) order is right for you. This is a medical order written by a doctor that informs healthcare providers not to perform cardiopulmonary resuscitation (CPR) if your heart stops beating. Similarly, a do-not-intubate (DNI) order tells the healthcare team that you don’t want to be put on a ventilator if your breathing stops.

Organ and tissue donations You may want to specify that you want to donate your organs, tissues, or both for transplantation. You may be kept on life-sustaining treatment temporarily while they’re removed for donation. To avoid any confusion, consider stating in your advance directive that you are aware of the need for this temporary intervention.

Visitors You may wish to make it known in advance who will be able to see you and when. This may include a visit from a religious leader. For some people, such a visit can provide a sense of peace.

Even if you write advance directives, it’s a good idea to discuss them with everyone involved in your care. “There is no substitute for meaningful conversations with loved ones and medical providers about one’s care goals and preferences,” says Dr. Shoemaker.

The advance directives can also specify if you would like to receive palliative care.

Choose Palliative Care

“Palliative care provides symptom control and supportive care along the entire disease continuum, from diagnosis of advanced cancer until the end of life,” says David Hui, MD, the director of supportive and palliative care research at MD Anderson Cancer Center in Houston.

It treats a range of symptoms and stress issues such as pain, fatigue, anxiety, depression, nausea, loss of appetite, and nutrition.

“We generally advise that patients with advanced cancer gain access to specialist palliative care in a timely manner to help them with their symptom management, quality of life, and decision-making early in the illness trajectory,” says Dr. Hui.

The goal of this approach is to provide an extra layer of support not only for the patient but for loved ones as well, especially family caregivers, according to the Center to Advance Palliative Care. It is appropriate at any age and at any stage of a serious illness, and you can receive it along with curative treatment.

Consider Hospice Care

Hospice care is one branch of palliative care. It delivers medical care for people who are expected to live for six months or less, according to the Hospice Foundation of America.

You may decide to consider hospice when there is a major decline in your physical or mental status, or both, despite medical treatment. Symptoms may include increased pain, significant weight loss, extreme fatigue, shortness of breath, or weakness.

Hospice can help you live with greater comfort if you decide to stop aggressive treatments that may have weakened you physically without curing your cancer or preventing it from spreading. Hospice care does not provide curative therapies or medical intervention that is intended to extend life.

A hospice care team often includes professionals from different disciplines, such as a doctor, nurse, social worker, chaplain, and home health aide. This team can guide you in managing your physical, psychosocial, and spiritual needs. They also support family members and other close unpaid caregivers.

Find Comfort at the End of Life

Finally, remember that end-of-life planning isn’t solely about medical care. It’s also a time when you will need emotional support. So, consider mending broken relationships, surrounding yourself with pictures of family and friends, and playing music that soothes your soul.

“People can write letters to loved ones, forgiving them or reconciling,” Redard says.

End-of-life planning is a topic people tend to shy away from, but it removes the burden from those left behind. “Once it’s over,” says Redard, “there’s relief.”

Readers blamed the predominantly for-profit nature of American medicine and the long-term care industry for systematically depleting the financial resources of older people.

Thousands of people shared their experiences and related to the financial drain on families portrayed in the Dying Broke series.

Thousands of readers reacted to the articles in the Dying Broke series about the financial burden of long-term care in the United States. They offered their assessments for the government and market failures that have drained the lifetime savings of so many American families. And some offered possible solutions.

In more than 4,200 comments, readers of all ages shared their struggles in caring for spouses, older parents and grandparents. They expressed their own anxieties about getting older and needing help to stay at home or in institutions like nursing homes or assisted-living facilities.

Many suggested changes to U.S. policy, like expanding the government’s payments for care and allowing more immigrants to stay in the country to help meet the demand for workers. Some even said they would rather end their lives than become a financial burden to their children.

Many readers blamed the predominantly for-profit nature of American medicine and the long-term care industry for depleting the financial resources of older people, leaving the federal-state Medicaid programs to take care of them once they were destitute.

“It is incorrect to say the money isn’t there to pay for elder care,” Jim Castrone, 72, a retired financial controller from Placitas, N.M., commented. “It’s there, in the form of profits that accrue to the owners of these facilities.”

“It is a system of wealth transference from the middle class and the poor to the owners of for-profit medical care, including hospitals and the long-term care facilities outlined in this article, underwritten by the government,” he added.

But other readers pointed to insurance policies that, despite limitations, had helped them pay for services. And some relayed their concerns that Americans were not saving enough and were unprepared to take care of themselves as they aged.

“It was a long, lonely job, a sad job, an uphill climb.”

Marsha Moyer

What other nations provide

Other countries’ treatment of their older citizens was repeatedly mentioned. Readers contrasted the care they observed older people receiving in foreign countries with the treatment in the United States, which spends less on long-term care as a portion of its gross domestic product than do most wealthy nations.

Marsha Moyer, 75, a retired teaching assistant from Memphis, said she spent 12 years as a caregiver for her parents in San Diego County and another six for her husband. While they had advantages many don’t, Ms. Moyer said, “it was a long, lonely job, a sad job, an uphill climb.”

In contrast, her sister-in-law’s mother lived to 103 in a “fully funded, lovely elder care home” in Denmark during her last five years. “My sister-in-law didn’t have to choose between her own life, her career and helping her healthy but very old mother,” Ms. Moyer said. “She could have both. I had to choose.”

Birgit Rosenberg, 58, a software developer from Southampton, Pa., said her mother had end-stage dementia and had been in a nursing home in Germany for more than two years. “The cost for her absolutely excellent care in a cheerful, clean facility is her pittance of Social Security, about $180 a month,” she said. “A friend recently had to put her mother into a nursing home here in the U.S. Twice, when visiting, she has found her mother on the floor in her room, where she had been for who knows how long.”

Birgit Rosenberg, 58, of Southampton, Pa.

Brad and Carol Burns moved from Fort Worth, Texas, in 2019 to Chapala, Jalisco, in Mexico, dumping their $650 a month long-term care policy because care is so much more affordable south of the border. Mr. Burns, 63, a retired pharmaceutical researcher, said his mother lived just a few miles away in a memory care facility that costs $2,050 a month, which she can afford with her Social Security payments and an annuity. She is receiving “amazing” care, he said.

“As a reminder, most people in Mexico cannot afford the care we find affordable and that makes me sad,” he said. “But their care for us is amazing, all health care, here, actually. At her home, my mom, they address her as Mom or Barbarita, little Barbara.”

Insurance policies debated

Many, many readers said they could relate to problems with long-term care insurance policies, and their soaring costs. Some who hold such policies said they provided comfort for a possible worst-case scenario while others castigated insurers for making it difficult to access benefits.

“They really make you work for the money, and you’d better have someone available who can call them and work on the endless and ever-changing paperwork,” said Janet Blanding, 62, a technical writer from Fancy Gap, Va.

Derek Sippel, 47, a registered nurse from Naples, Fla., cited the $11,000 monthly cost of his mother’s nursing home care for dementia as the reason he bought a policy. He said he pays about $195 a month with a lifetime benefit of $350,000. “I may never need to use the benefit(s), but it makes me feel better knowing that I have it if I need it,” he wrote. He said he could not make that kind of money by investing on his own.

“It’s the risk you take with any kind of insurance,” he said. “I don’t want to be a burden on anyone.”

Pleas for more immigrant workers

One solution that readers proposed was to increase the number of immigrants allowed into the country to help address the chronic shortage of long-term care workers. Larry Cretan, 73, a retired bank executive from Woodside, Calif., said that over time, his parents had six caretakers who were immigrants. “There is no magic bullet,” he said, “but one obvious step — hello people — we need more immigrants! Who do you think does most of this work?”

Victoria Raab, 67, a retired copy editor from New York, said that many older Americans must use paid help because their grown children live far away. Her parents and some of their peers rely on immigrants from the Philippines and Eritrea, she said, “working loosely within the margins of labor regulations.”

“These exemplary populations should be able to fill caretaker roles transparently in exchange for citizenship because they are an obvious and invaluable asset to a difficult profession that lacks American workers of their skill and positive cultural attitudes toward the elderly,” Ms. Raab said.

“For too many, the answer is, ‘How can we hide assets and make the government pay?’”

Mark Dennen

Federal fixes sought

Others called for the federal government to create a comprehensive national long-term care system, as some other countries have. In the United States, federal and state programs that finance long-term care are mainly available only to the very poor. For middle-class families, sustained subsidies for home care, for example, are fairly nonexistent.

“I am a geriatric nurse practitioner in New York and have seen this story time and time again,” Sarah Romanelli, 31, said. “My patients are shocked when we review the options and its costs. Medicaid can’t be the only option to pay for long-term care. Congress needs to act to establish a better system for middle-class Americans to finance long-term care,” she said.

John Reeder, 76, a retired federal economist from Arlington, Va., called for a federal single-payer system “from birth to senior care in which we all pay and profit-making removed.”

John Reeder, 76, at home in Arlington, Va.

Mark Dennen, 69, from West Harwich, Mass., said people should save more rather than expect taxpayers to bail them out. “For too many, the answer is, ‘How can we hide assets and make the government pay?’ That is just another way of saying, ‘How can I make somebody else pay my bills?’” he said, adding: “We don’t need the latest phone/car/clothes, but we will need long-term care. Choices.”

<h2″>Questioning life-prolonging procedures

A number of readers condemned the country’s medical culture for pushing expensive surgeries and other procedures that do little to improve the quality of people’s few remaining years.

Dr. Thomas Thuene, 60, a consultant in Roslindale, Mass., described how a friend’s mother who had heart failure was repeatedly sent from the elder care facility where she lived to the hospital and back, via ambulance. “There was no arguing with the care facility,” he said. “However, the moment all her money was gone, the facility gently nudged my friend to think of end-of-life care for his mother. It seems the financial ruin is baked into the system.”

Joan Chambers, 69, an architectural draftsperson from Southold, N.Y., said that during a hospitalization on a cardiac unit she observed many fellow patients “bedridden with empty eyes,” awaiting implants of stents and pacemakers.

“I don’t want to be a burden on anyone.”

Derek Sippel

“I realized then and there that we are not patients, we are commodities,” she said. “Most of us will die from heart failure. It will take courage for a family member to refuse a ‘simple’ procedure that will keep a loved one’s heart beating for a few more years but we have to stop this cruelty.

“We have to remember that even though we are grateful to our health care professionals, they are not our friends, they are our employees and we can say no.”

One physician, Dr. James D. Sullivan, 64, from Cataumet, Mass., said he planned to refuse hospitalization and other extraordinary measures if he suffered from dementia. “We spend billions of dollars, and a lot of heartache, treating demented people for pneumonia, urinary tract infections, cancers, things that are going to kill them sooner or later, for no meaningful benefit,” Dr. Sullivan said. “I would not want my son to spend his good years, and money, helping to maintain me alive if I don’t even know what’s going on,” he said.

Thoughts on assisted dying

Others went further, declaring they would rather arrange for their own deaths rather than suffer in greatly diminished capacity. “My long-term care plan is simple,” said Karen D. Clodfelter, 65, a library assistant from St. Louis. “When the money runs out I will take myself out of the picture.” Ms. Clodfelter said she helped care for her mother until her death at 101. “I’ve seen extreme old age,” she said, “and I’m not interested in going there.”

Some suggested that assisted dying should be a more widely available option in a country that takes such poor care of its elderly. Meridee Wendell, 76, from Sunnyvale, Calif., said: “If we can’t manage to provide assisted living to our fellow Americans, could we at least offer assisted dying? At least some of us would see it as a desirable solution.”