Many people delay the conversation or thoughts of having to prepare a will. Confronting the possibility of one’s death is not easy. However, as the recent death of Anne Heche shows us, not having a will can place a significant burden on your children and cause undesirable complications. Even if difficult, planning ahead may be a better solution than the alternative.

What Happened With Actress Anne Heche?

Anne Heche’s case is a good example of why a person may want to consider creating a will sooner rather than later. Heche was divorced with two children from different relationships when she passed away. Her eldest son is 20 years old, but her younger son is still a minor.

Although they are assumed to be her sole heirs, only her oldest son is of age to administer her estate. He has filed a petition for a guardian ad litem to be put in place to protect his younger brother’s interests. The guardian ad litem may be a financial burden to Heche’s estate, and the costs of securing this professional will potentially reduce the assets available to her sons.

Even though her eldest son is dealing with his mother’s estate, this is undoubtedly very difficult for a person to go through at such a young age. Heche’s eldest son likely will not be able to do this all on his own and will need the services of a probate attorney — likely further increasing the costs of administering her estate and depleting how much is left for her children.

It has also been reported that an inventory and appraisal of her estate is needed to determine its worth and what assets she had. This process requires further professional involvement and fees that her estate must pay. In addition, it is possible that the father of her youngest son may seek to intervene in the estate’s administration to ensure he is treated fairly. Litigation costs could rack up quickly if there is any disagreement related to this.

Preparing a will and other estate planning documents can make legal proceedings significantly less complex and expensive and keep your situation as private as possible. It can also make it easier for your loved ones to know exactly what you want to happen to your assets and possessions.

Who Inherits When You Die Without a Will?

Many people do not realize that if you pass away without a will, your local state laws on intestacy will determine who qualifies as your heirs and inherits your property.

For example, in many states, if a person passes away unmarried but with children, the children will inherit everything. But what if the person had a long-term partner or was engaged to be married? They may have wanted their significant other to inherit some of their assets, but a “default” state law may lead to a different result. Or, what if you have no living children, siblings, parents, or spouse? Your property may go to the government instead of friends, grandchildren, nieces, or nephews. Having a will prevents these scenarios from happening.

Choose a Guardian for Your Children

Another benefit parents should consider is their ability to choose a guardian for their children in advance.

This matters, for example, when the other parent is not living or cannot be located. If a person does not set forth their wishes ahead of time, multiple parties may step up after a person’s death and argue over who should care for any minor children.

A court may be tasked with making this decision, and it may not be what you would have wanted. This can be expensive, traumatic for all involved, and a long process. Courts will generally try to appoint the individual a person has selected if your wishes are in a will or other planning document.

The Bottom Line

The bottom line is that having estate planning documents in place makes your wishes more likely to be honored and less likely that a court will decide what happens. This is also true where you may be incapacitated and unable to voice your wishes. While Anne Heche’s situation is not unusual, it is avoidable.

11 End of Life Documents for Mesothelioma & Cancer Patients

Although patients can outlive a prognosis and even reach remission, mesothelioma remains one of the worlds most deadly conditions. This is why mesothelioma patients should take as many measures as possible to ensure their personal finances and responsibilities are covered. Many people have a will prepared, but there are several other end of life documents that are essential family members or patients dealing with mesothelioma. Without these kind of documents, loved ones will have to make difficult decisions on your behalf with no guidance. Although it may be difficult to discuss, Mesothelioma Hub feels it is still necessary to prepare for the worse. Here is our list of eleven essential documents that all families should prepare while dealing with a mesothelioma prognosis.

1) Letter of Competency

A letter of competency is one of the first end of life documents to complete during your planning. A letter of competency is a statement from a mesothelioma doctor or specialist stating that a person is capable of making informed, stable decisions. This end of life document could apply to health care, finances, or estate. A common side effect of mesothelioma treatment is memory loss, confusion, and brain fog. Therefore, it is essential to obtain a letter of competency if applicable.

2) Living Trust End of Life Document

A living trust is another essential piece of end-of-life paperwork. A trust is created and funded during a patient’s lifetime that they can amend or revoke as time goes on. A living trust appoints a person or corporation to act as a “trustee” after their passing. The document also designates the “beneficiaries,” aka the people who receive income or other property from the trust. This trustee manages the trust property for the benefit of the beneficiaries.

The average lifespan for a mesothelioma patient after receiving a diagnosis is 4 – 18 months. A living trust is an end of life document that you should assemble as quickly and efficiently as possible during your end-of-life preparation and especially during the more advanced terminal stages.

3) Last Will and Testament

A last will and testament is the legal end of life document specifying a patient’s last wishes pertaining to assets and dependents after death. Although similar to a living trust, the last will controls property directly under the control of the individual and does not include jointly owned assets whereas a living trust controls all assets. Details included in the last will and testament include what to do with possessions, and what will happen with their responsibilities including dependents and management of financials.

4) Letter of Intent

Although not a legal document, a letter of intent can be beneficial for your executor and family members. A letter of intent can act as an end-of-life checklist for your loved ones for wishes not covered in a will. The document can include the location of important legal end of life documents, names and contacts, care for pets, and many more details. It should remain a high priority for those with wishes that can’t be fully explained within other documents.

5) Financial Power of Attorney

The purpose of a financial power of attorney is to designate an agent to handle financial affairs. This person has the legal ability to make decisions about a person’s finances when someone is ill, disabled, or physically not present. The agent should make arrangements in line with the person’s wishes but has full authority to make autonomous decisions until their authority is challenged or revoked by the law.

Many people on their life journey were negligently exposed to asbestos and developed mesothelioma. This is where your a financial power of attorney can come in and assist with the legal side of things and even pursue legal help and compensation.

Need to Obtain End of Life Documents?

A late stage mesothelioma diagnosis can bring up difficult questions. Request an evaluation and let us help you with your case. Evaluate My Case

6) Health Care Power of Attorney

If a patient is unable to make medical decisions for themselves, they may choose to have a health care power of attorney. A health care agent should be someone trustworthy and noble as they can:

Accept, withdraw, or decline treatment

Agree to admit or discharge a patient from any medical center or institution

Access medical and mental health records and share them with others

Carry out plans or make decisions about the body or remains

Throughout the mesothelioma journey, several health-related decisions will need to be made. Whether you are going through treatment or are staying in an assisted living home, a health care power of attorney can assist you in these decisions and maintain important end of life documents.

7) Living Will End of Life Document

A living will is a vital facet of a patient’s end-of-life plans. This document declares a patient’s desire to have death-delaying procedures withheld after being diagnosed with a terminal illness. This end of life document can assist doctors and loved ones if a decision needs to be made about withholding death-delaying procedures.

The medical community considers mesothelioma a terminal illness. If you are interested in death-delaying procedures being withheld, you should complete a living will.

8) Organ Donor Care

Those interested in donating their organs should complete a health care directive stating their wishes. If arrangements have already been made, specifying an end of life document should include all necessary information. If a patient has a health care agent, they can also make the decision with guidance from the patient.

9) HIPAA Release

Health care information of everyone is not accessible by others before or after their death. However, a HIPAA release form shares otherwise protected health information with other individuals or organizations. Patients should file a HIPAA release form if they would like their health care agents or loved ones to have access to their important end of life medical details.

10) DNR Order End of Life Document

A health care provider will typically begin CPR and life-saving activities if the heart or breathing stops, however, people can choose to not receive care under these circumstances. A do not resuscitate (DNR) order states that a patient prefers to not receive CPR in the case that the heart or breathing stops.

Many mesothelioma patients that pass, developed the condition due to negligence. The patient’s loved ones may be eligible to file a wrongful death suit against the individual or company believed to be responsible for negligence. Thats why it’s so important for to keep all your family members end of life documents secured and organized.

11) Digital Asset Instructions

Nowadays, the average person has almost 200 digital accounts including bank, investment, insurance, cryptocurrency, and social accounts. Some of these accounts, if not all, will need attention after a person passes. If these accounts are password protected, a patient should assemble a list of login information. Patients can even assign a digital executor to manage online accounts after they pass.

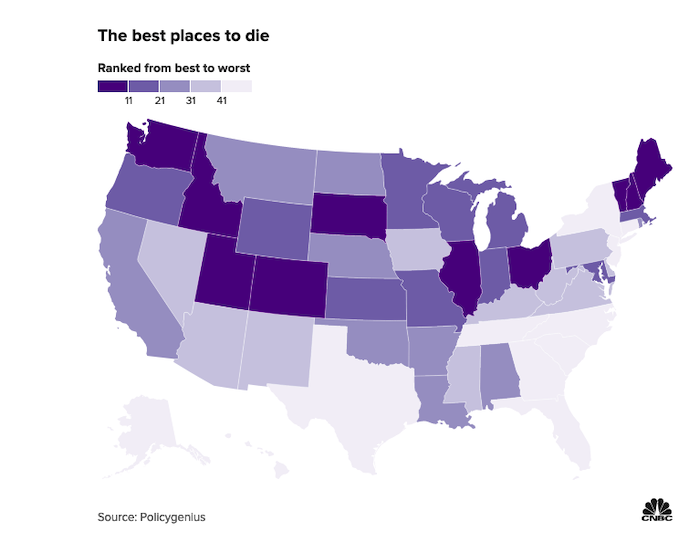

Your end-of-life experience may be very different depending on where you live, according to a Policygenius report.

The report ranks the best and worst U.S. places to die based on funeral costs and services, green burials, palliative care, Medicare providers, at-home deaths and probate shortcuts.

Your end-of-life experience may be very different depending on where you live, according to a Policygenius report that ranks the country’s best and worst places to die.

The report gave each state and the District of Columbia a numerical score based on seven factors, including funeral costs and services, green burials, palliative care, Medicare providers, at-home deaths and probate shortcuts.

“I think the big takeaway of this project is to get people thinking about the costs associated with the end of life,” said Logan Sachon, senior managing editor of research at Policygenius. “Because some of them can be mitigated through planning.”

“If you look at the top 10 and bottom 10, there aren’t any specific things they all have in common,” Sachon said. “They are each kind of unique in their own way.”

Indeed, Vermont, ranked as the No. 1 place to die, was among the most expensive for funeral costs but scored highest for palliative care, which focuses on pain relief, management and emotional support.

Florida, known for its high population of retirees, came in last place, with the fewest Medicare providers per capita, and scored low for at-home deaths and palliative care.

The best places in the U.S. to die

Vermont

Utah

Idaho

Ohio

South Dakota

Maine

Colorado (tie)

Illinois (tie)

New Hampshire

Washington

The worst places in the U.S. to die

Florida

Alaska

Texas

Hawaii

New York

Georgia

New Jersey

North Carolina

South Carolina

Connecticut

It’s never too early for older Americans to prepare for end of life, Sachon said.

Experts recommend an advanced directive, also known as a living will, covering your medical care preferences. You’ll also need a health-care proxy or power of attorney, naming someone to make medical decisions on your behalf if needed.

Estate planning

The report also focuses on each state’s probate process, which determines the cost and time it takes to settle your estate.

As of June 2021, only 17 states and the District of Columbia have an estate or inheritance tax, according to the Center on Budget and Policy Priorities.

With different laws in every state, a local estate planning attorney may share some options to protect your assets and carry out your wishes, depending on where you live.

There’s no federal estate tax on wealth below $12.06 million for individuals in 2022, and with proper planning, married couples can transfer their unused exemption to their surviving spouse, effectively doubling it to $24.12 million.

However, this reverts to an estimated $6 million exemption in 2026 when provisions from the Tax Cuts and Jobs Act sunset.

As a thing that most people try to avoid, death isn’t a common topic of conversation. After all, discussing it requires confronting its inherent inevitably—but avoiding discussions surrounding it doesn’t just bring blissful ignorance, either. In fact, this tactic can leave your loved ones in the lurch when death does arrive. That’s why estate-planning attorneys suggest considering in advance how you’ll discuss your plans for death with your family, and above all, making a point to do so.

Death comes along with an emotional and logistical cascade of concerns for those close to the person who passed. While working with a palliative-care professional or death doula once death becomes imminent can certainly help with the emotional side of things, creating an estate plan ahead of time mitigates stress related to the logistics. “This is why we always say every adult should have a will,” says estate-planning attorney Rosalyn Carothers, JD. “For one, that allows you to direct what happens to any of your assets, and two, you’re making it easier and less expensive for your family members to help, as you’d have seen fit.”

“If you indicate clearly [to family members], ‘Here is my plan,’ then everyone can get on the same page, and it’s harder for someone to feel like they’re getting cheated.” —Patrick Hicks, JD, general counsel at Trust & Will

But, because of the inherent sensitivity of a will—deciding who gets what and what goes where—creating one only gets you halfway to solid death preparations. Learning how to discuss your plans for death with loved ones is the other half, both so that they know exactly where to find all the relevant documents in the event of death, and also so that they can help ensure your wishes are carried out effectively, without confusion, disagreement, or unwelcome surprises. “If you indicate clearly, ‘Here is my plan,’ then everyone can get on the same page, and it’s harder for someone to feel like they’re getting cheated, so to speak, when push comes to shove,” says estate planning attorney Patrick Hicks, JD, general counsel at Trust & Will.

Below, estate-planning attorneys share the key elements of end-of-life planning to talk about explicitly with family members, so that everyone knows what to expect should the unexpected occur.

What to discuss with family about end-of-life issues, according to estate planning attorneys

1. End-of-life wishes

A handful of both pre- and post-death desires fit into this category—which covers what you’d like to happen in the event that you’re incapacitated or terminally ill (the details of which can be legalized in a living will) and how you’d like your body to be handled should you pass (like your preferences for burial or cremation, for instance). “You really want to let folks in your life know, ‘Hey, if I’m in this circumstance, do this or don’t do this,’ regarding life support, in particular, so that loved ones feel like they are intimately aware of what you would’ve wanted,” says Carothers.

Even if it’s all legally delineated in your estate plan, talking about these desires openly can spare the people in your life who survive you from some very difficult conversations, says Hicks. It’s also worth mentioning that, in the same conversation, you should tell loved ones exactly where they can find the documents detailing these wishes, so that there’s no need to search for them if and when the time comes.

2. Who will handle what when death nears

Once you start considering your plans for death, you’ll quickly run up against what Carothers calls the “who’s its” and the “what’s its.” This refers to “who” in your life is going to handle “what,” logistically speaking, when you’re about to pass and afterward—which is another big source of potential death-related conflict that can often be avoided with a conversation.

The most contentious roles to consider are who you’ll appoint as your financial and health-care agents under your powers of attorney, or the person (or people) you’re choosing to handle your finances and taxes and your medical decisions, respectively, whenever you become unable to do so. “Sometimes, people don’t want to speak to their kids or siblings about this because they don’t want to hurt anybody’s feelings,” says Carothers. “But, it’s better to let these loved ones know upfront who you’re choosing for what and why.” That way, there’s less chance of a dispute after the fact.

The same goes for clarifying whom you’ll be naming as the executor of your estate (once you have a will in place or while you’re creating one). This is the person who will settle your accounts, manage your personal assets, and disseminate the right assets to the designated beneficiaries of your will after you pass. Talking about this with family members lets everyone know whom they should turn to for any will-related matters post-death.

3. People to call in the event of an accident

Chances are, you may not even know exactly who among a parent or sibling’s friends or acquaintances you should contact directly should they become incapacitated or die. And if you do, it’s even likelier that you don’t have their contact info handy. “Nowadays, everything is just saved in everybody’s cell phones, but what happens if you lose a loved one’s phone in an accident or you just can’t unlock it?” says Carothers.

That’s why she suggests everyone keep a list of the few close friends whom they’d like to be contacted should something happen to them, along with their contact information, and inform loved ones where they can find it in the event of an accident. Also on that list should be the name and contact info of your accountant and homeowner’s insurance agent, if either or both applies, adds Carothers, since these are usually the most important people to reach in any situation where someone is nearing death.

4. Sentimental assets

Surprisingly, it’s often the sentimental pieces of property that tend to create the most tension among a decedent’s family members, says Hicks. “With valuable assets, a lot of the time, it gets quickly resolved, either according to the specific plan in place, or in a way where things get divided equally,” he says. “But it’s the things that don’t have a lot of economic value, but that have sentimental value which are typically not accounted for in a will, and then get fought over.”

That could mean a family photo album, an antique, a special piece of artwork, or any other kind of family heirloom that can’t just be cut up into parts and divided equally. “Not having a conversation upfront about who’s going to get which of these items often leads to disputes and disagreements,” Hicks says. Talking explicitly about sentimental pieces in advance can certainly get ahead of these potential arguments, though Carothers also suggests checking to see if your state allows you to file a memorandum along with your will that can include a written file of all these items, listing the person’s name to whom each should go.

Since the outbreak of the Covid-19 pandemic, the virus has spread worldwide like wildfire, and millions of people have been affected by the unexpected death of a loved one. Nobody wants to think about death, but ask yourself this question right now – what if I were to die today? Would your loved ones be plunged into chaos and uncertainty and have to deal with this on top of the trauma of your passing?

In order to protect your loved ones from this harsh reality, you might want to apply the following practical guidelines while you’re still alive.

It is essential to ensure that all your affairs are in order, to avoid your spouse and family or your next of kin having to scurry around in the event of your death.

Put together a “life file” that contains all your important documents and information, along with a full list of, for example, your assets and liabilities, credit insurance, policies, usernames and passwords, as well as your executor and financial advisor’s contact details.

Ensure that you have a valid will in place.

Should you not wish to be kept alive artificially you might consider having a living will drawn up. A living will is an instruction to medical practitioners and your next of kin regarding your wishes if the difficult decision to turn off the machines that are keeping you alive must be taken. If you are a registered organ donor, you can also put this fact on record in your living will.

Your loved ones need to be aware of your wishes regarding cremation or burial, the details of any funeral cover you may have, and whom to contact when the inevitable happens.

The suggestions that follow might sound trivial, but make sure your spouse and family know how everything works in and around the house.

Be certain that your spouse has access to sufficient funds to cover all expenses for at least six to eight months. Most of us are aware of the challenges facing the Master’s offices nationwide, and estates are taking longer to be wound up.

Your spouse needs to start building up their own credit record in your lifetime to be able to qualify for services and utilities, a cell phone contract, a mortgage or a hire purchase agreement after your death, if not already.

Check that beneficiaries have been nominated for all your life policies, where necessary, and that nomination forms have been completed in respect of any annuities and group insurance you may have.

It is a good idea for your spouse to meet with your financial advisor and start building a relationship of trust between them so that the advisor can provide professional advice on your spouse’s future once you are longer there.

Have business continuity discussions with partners / next of kin to manage continuity and risks.

Ensure liquidity in the estate to pay administration costs, liabilities and taxes that will become due.

Using the above basic guidelines will have a positive effect and make the transition easier for all concerned.

Some guidelines for the surviving spouse to manage financial expectations:

Adequate funds are unlikely to be a major problem for your surviving spouse if you have managed your affairs well during your lifetime. This includes having made provision for life insurance so that there will be sufficient income to cover the expenses, as well as having set up a network of competent and reliable people to provide your spouse with professional advice.

If the surviving spouse is in the unfortunate position of having insufficient funds, careful planning must be done to provide for the basic expenses such as rent or a mortgage, as well as utility bills, food and insurance premiums.

It is important for your spouse to receive advice from a financial advisor – one with whom a good relationship has already been established – on investments, cash flow and how a basic budget (income and expenses) work. The financial advisor will assist here with a new plan to secure your spouse’s future.

Don’t be in a rush to make major financial decisions straight away. Something that sounds like a good idea right now will not necessarily seem so wise in six months or a year.

People are living longer and provisions must be made for the available funds to generate an adequate income. Ensure that the quantum of life insurance is determined in line with a properly prepared cash flow projection.

A surviving spouse should update their will in order to make provision for guardians, trusts and the like.

People often make poor financial decisions during the mourning process and therefore it is important to obtain reliable professional advice ahead of time in order to help you make well-informed choices, both for your benefit and for your family’s future.

Loss of a loved one is a difficult time to navigate. Learn how to obtain a death certificate, when to begin reporting the death and more.

Key takeaways:

Grief is a natural part of losing a loved one. Having an after-death checklist can take a tremendous burden off your shoulders when it comes time to execute final wishes.

Besides making funeral arrangements, you will have to determine if there was a will, report the death to various entities and close financial accounts.

You will need certified copies of death certificates to claim the deceased person’s assets, including life insurance policies and brokerage accounts.

Everyone experiences loss at one point or another in life. It’s natural. However, many people underestimate the amount of paperwork involved to settle their loved one’s affairs. From making funeral arrangements to obtaining death certificates, the process can be stressful if you don’t know where to start.

Having a plan in place can help you better navigate this difficult time. You should also reach out to family members and consider obtaining the help of lawyers and certified public accountants (CPAs) to ensure you don’t have to handle everything on your own.

We’ve put together a checklist to help you prioritize your tasks and delegate where needed.

After-Death Checklist: A Guide To Managing Your Loved Ones Death

It can be overwhelming trying to figure out what to do when a loved one dies. Having an after-death checklist can lessen the burden.

Here are some key steps to consider when a loved one dies:

Acquire a pronouncement of death

Alert friends and family

Implement burial plans (based on will or last wishes)

Report death to Social Security and other government agencies

Obtain certified copies of death certificate

Identify all assets and liabilities

File insurance claims

Determine if there was a will

Close bank and brokerage accounts

Send copies of death certificate to major credit agencies

Terminate memberships and subscriptions that are not in use

Terminate health insurance policies

Settle a loved one’s outstanding financial debts

Notify election office of death

Remember that timing may vary depending on your circumstances. If this was an unexpected death, it may take longer to access all the required information to begin the final arrangements. This is another reason why planning early is important.

Immediately Following The Death Of A Loved One

The first task on your list will be to obtain a legal pronouncement of death. If your loved one died in a hospital, a staff member will provide you with a pronouncement of death form.

The process is different for deaths that occur in the home. You will need to call a medical professional to pronounce them deceased.

Next, you want to alert friends and family of the death. Send out text messages or share on social media to spread the word. Remember to take a careful approach during this step. Use your judgment to determine the best way of informing those who need to know.

What To Do Within The First Week Of Losing A Loved One

The first week can be a whirlwind of emotions and roadblocks without a proper plan in place. Here are some steps you can take to better manage your priorities.

Make funeral arrangements

Your loved one may have recommended what they wish for their last requests. This may include burial and estate planning. Contact their funeral home, make the burial arrangements and determine if there was a prepaid burial plan in place.

If your loved one did not share their last wishes, it might be best to reach out to close family or friends for assistance. Research funeral prices and outline the expected costs. Then, determine how you will pay for the funeral. The Department of Veterans Affairs offers burial benefits for qualified individuals.

Report death to Social Security and other government agencies

The funeral home usually reports a person’s death. If you need to report it yourself, you’ll need to call the Social Security office at 1-800-772-1213 (TTY 1-800-325-0778).

Obtain certified copies of death certificate

You can contact the Vital Records office of the state where your loved one died to obtain copies of the death certificate. You’ll need the certified death certificate to file insurance claims and access bank accounts. You can request at least 5-10 copies of the death certificate. It all depends on the number of assets that your loved one held.

Identify all assets and liabilities

You typically need certified copies of the death certificate to claim assets that may be in your loved one’s name. Here are a few types of assets that you may need to inquire about:

Deeds and titles

Insurance policies

Safety deposit boxes

Brokerage accounts

Employer benefits

Retirement assets

You probably won’t be responsible for any outstanding debt that your loved one left behind. If you co-signed on any type of asset or debt that has gone unpaid, you may be responsible. Many in the family mistake debt as “inherited” when this is not always the case. Money from the estate is used to pay the debt. State laws on inheriting debt may vary, but liabilities commonly go unpaid if there isn’t enough from the estate to pay the debt.

File insurance claims

Reach out to your loved one’s life insurance provider to submit a claim. Here’s the standard process:

Contact the insurance company and inform them about the death.

The insurance provider will send a packet of forms and instructions to follow.

Submit the death certificate and completed forms.

The insurer usually pays claims within 30 to 60 days of receiving all requested information.

Determine if there was a will

A will can help you determine how assets should be allocated. It can also help you manage any other requests that your loved one may have had. This includes identifying the executor of your loved one’s estate. The executor is the person appointed to carry out the instructions of the will.

Here are some items to consider:

An executor files the will with the probate court. You can consult with an estate attorney for guidance. An executor typically has a limited number of dates to submit this. Check with your probate court for more information.

Wills become public record once they have been processed through the County Clerk’s office.

The executor must notify the appropriate authorities about the death.

If your loved one died without a will, your state law will determine how assets are managed.

Within The First Month Of Losing A Loved One

There are steps of action that should be taken within the first month following the loss of a loved one. These can vary, depending on how much was prepared initially and where the loved one passed. However, this is a great baseline to follow if you’re unsure.

Close bank and brokerage accounts.

Identify all financial accounts in your loved one’s name. Notify the institutions about the death and provide a certified copy of the death certificate. They will release the funds to the beneficiaries on the account.

Send copies of the death certificate to major credit agencies.

The three major credit-reporting agencies in the U.S. are Equifax, Experian and TransUnion. Report your loved one’s death to the credit agencies to prevent any fraudulent activity. You can find their contact information by visiting the Federal Trade Commission’s consumer information.

Terminate memberships and subscriptions that are not in use.

Check mail, email and bank statements to identify gym memberships or digital subscriptions that need to be canceled. Have account or member ID numbers handy to expedite the process.

Terminate health insurance policies.

If you haven’t already, now is the time to file a claim with your health insurance to ensure the policy has been closed upon the death of a loved one. Contacting the insurance agency should be the best way to get in contact with the claims department and start this process.

Settling a loved one’s outstanding financial debts.

Repaying debts falls on the deceased person’s estate. This is not the responsibility of a particular family member. However, the executor or power of attorney is responsible for paying these debts using money from the estate. This is done by selling assets or using any other funds provided by the estate.

Notify the election office of death.

Notifying the election office of a death does not fall on you directly, as a family member of the deceased. Once you’ve filed for a death certificate, this record is then used to remove deceased participants from the voter registration list.

Who Gets The $255 Social Security Death Benefit?

The Social Security Administration (SSA) provides a lump-sum payout of $255 to qualified individuals following the death of a loved one. In order to receive this benefit, you must first apply by calling the Social Security office at 800-772-1213. The following individuals may qualify if they meet criteria outlined by the SSA:

Surviving spouse

A widow

A surviving divorced spouse

An eligible child

What Happens To A Person’s Estate After They Die?

If your loved one has an estate plan, it can save you or a loved one from financial loss or litigation on settling an estate. The estate plan helps families determine what happens after a loved one dies. It typically includes the following items:

Will

Executor

Healthcare directives

Beneficiary designations

If there is no estate plan, you’ll need to consult state law for details on who receives assets. Generally, it passes to parents, spouse, children or other relatives.

The Bottom Line

Saying goodbye to a loved one is difficult enough without the stress of sorting through paperwork. The best course of action is to identify the most important steps in the process and move forward from there. Take time to review wills, estate plans and life insurance policies. Don’t forget to seek out help and use the resources available to you. Consult family members and experts to avoid managing the process on your own.

As the coronavirus pandemic increased anxiety and upended many lives, it led U.S. millennials to get more serious about end-of-life planning.

According to new research from 1Password, a digital security and privacy platform based in Toronto, and digital estate planning platform partners Trust & Will and Willful, 72% of U.S. millennials (ages 25 to 40) with wills created them or updated them in the past year.

In addition, 34% of these millennials have talked about their digital assets with their parents in the past year.

More than two-thirds of millennials don’t have a will

While the pandemic brought greater focus to end-of-life planning among millennials, they’re still largely unprepared. According to the 1Password findings, 68% of millennials don’t have a will.

In turn, respondents estimate descendants would lose access to an average of $22,500. Plus, only 38% have clarity over who should handle their digital assets after they die.

Among those who do have a will, here’s what sparked it:

With a digital handover, the top priority for respondents is giving their executor login credentials to banking and financial accounts (67%). Interestingly, 57% of millennial respondents say granting access to social media accounts is more important than giving access to email, subscription and e-commerce accounts.

Navigating a post-death digital handover

The pandemic provided a wake-up call for millennials and their end-of-life planning, no doubt. But there are some areas of estate planning that are murky. And it’s not just about the respondents themselves.

The survey finds 51% of millennials will be responsible for the execution of their parents’ wills. However, just 36% have access to their parents’ online account passwords.

While we already noted that 34% of respondents say they’ve chatted with their parents about their digital assets in the past year, 52% have never discussed it with their parents or can’t recall the conversation. Among those who have handled the execution of wills, 63% say it was more challenging than expected to access accounts after a death.

Millennials use old-fashioned ways to store documents

Old-school ways of handling important documents reign supreme among the millennial crowd. More than 4 in 5 (81%) report keeping paperwork — think birth certificate — in a physical location like a safe deposit box, safe or filing cabinet.

They share their passwords mainly by way of a written list (41%), then verbally (39%) and digitally (25%), such as through email, Google Docs, the cloud or a PDF.

As for storing passwords, 51% say they store their passwords by memory, while 25% keep them on a piece of paper. One in 5 (20%) millennials say they use a password manager.

The report also found that 48% of millennials trust their significant others the most for emergency access to their passwords, more than twice as much as their second choice — their parents (20%).

If you’re prioritizing end-of-life planning, decide who will be granted access to your digital accounts and online passwords and list out all your debts. This might include: